“Don’t simply retire from something; have something to retire to.” -Harry Emerson Fosdick

Are you approaching retirement and wondering how to keep more of your hard-earned money? Tax-efficient withdrawal strategies are essential for minimizing your tax liability, maximizing your income during retirement, and improving your retirement score.

Get ready to explore various methods for withdrawing from different types of accounts—Traditional IRAs, Roth IRAs, 401(k)s, and taxable accounts—in a smart and tax-efficient way.

Key Takeaways

- Different accounts, different rules. Different types of retirement accounts—Traditional IRAs, Roth IRAs, and taxable accounts—have distinct tax implications and withdrawal rules, which are crucial for maximizing after-tax income during retirement.

- Extend your savings as much as you can. Strategic withdrawal tactics such as the 4% rule, proportional withdrawals, and the bucket strategy can help manage tax liability, stabilize income, and extend the longevity of retirement savings.

- Plan your strategies ahead. Effective tax management during retirement involves planning for timing withdrawals, utilizing tax-free income sources like HSAs and municipal bonds, and consulting tax professionals to optimize strategies and minimize liabilities.

Understanding Different Types of Retirement Accounts

Figuring out the tax impact of different retirement accounts is crucial for maximizing your after-tax income in retirement. Here’s the lowdown:

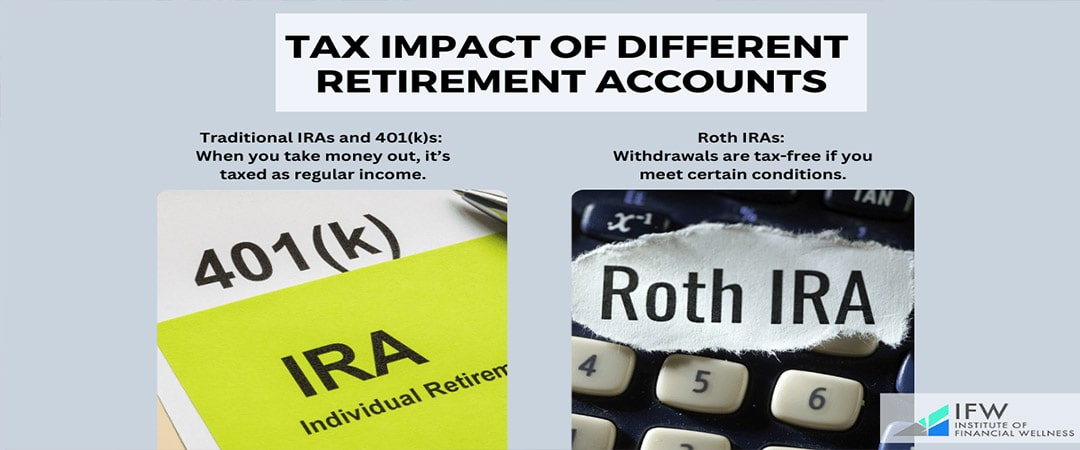

- Traditional IRAs and 401(k)s: When you take money out, it’s taxed as regular income.

- Roth IRAs: Withdrawals are tax-free if you meet certain conditions.

Even regular taxable accounts can play a big role in your retirement plan. A mix of different accounts keeps your finances flexible and can provide extra tax perks.

Traditional IRA and 401(k) Withdrawals

Watch out for taxes on traditional IRAs and 401(k)s! When you withdraw from Traditional IRAs and 401(k)s funded with pre-tax dollars, those withdrawals are taxed as regular income.

Every dollar you take out adds to your taxable income for the year, possibly bumping you into a higher tax bracket.

Once you hit 73, you must start taking Required Minimum Distributions (RMDs) from these accounts. If you don’t plan ahead, these RMDs can have a big impact on your taxes.

Roth IRA Withdrawals

So, are Roth IRAs a smart choice for retirement?

Roth IRAs let you withdraw money tax-free as long as the account has been open for at least five years and you meet the withdrawal rules. This makes Roth IRAs a great option for retirement savings because your retirement income from these accounts is free from federal taxes.

Plus, Roth IRAs don’t have required minimum distributions (RMDs), giving you more freedom to decide when and how much to take out. This flexibility can make tax planning easier and more effective.

Taxable Accounts

What are some smart tax moves for your taxable accounts? We can mention these:

- Balancing gains with losses

- Taking full advantage of tax deductions and credits

By doing this, you can reduce your overall tax bill and keep more of your hard-earned money. However, managing investments in taxable accounts comes with some important tax rules to keep in mind:

- Interest Income: This is taxed at your regular income tax rates.

- Capital Gains and Qualified Dividends: These get the benefit of lower long-term capital gains tax rates.

The 4% Rule: A Steady Income Plan for Retirees

The 4% withdrawal rule, introduced by financial adviser Bill Bengen in the 1990s, is a popular way to create steady income in retirement. Here’s how it works:

- Withdraw 4% of your total retirement savings in the first year.

- Increase that amount by 2% each year to keep up with inflation.

Based on historical market data, the 4% rule aims to give you a reliable income while keeping enough in your account for future years.

Pros and Cons of the 4% Rule

Why do many retirees love the 4% rule? It is popular among people in retirement because it’s simple and provides a steady income stream.

You can count on it like a pension or annuity, and it’s easy to follow.

However, sticking to the 4% rule means you can’t easily adjust to changes in your lifestyle or spending needs. Plus, since it’s based on past market performance, there’s a risk that if the markets don’t do well, you could run out of money sooner than expected.

Proportional Withdrawal: A Smart Way to Manage Retirement Funds

Another way to reduce taxes when withdrawing money is by doing proportional withdrawals. This way, you can:

- Take money from different types of accounts at the same time to spread out your tax burden.

- Aim to keep your tax bill steady throughout retirement.

- Could end up paying less in taxes overall and boost your after-tax income.

By strategically withdrawing equal amounts from taxable, tax-deferred, and Roth accounts, you can reduce your overall tax impact and make your retirement savings last longer.

We can also mention some advantages of utilizing a proportional withdrawal approach, such as:

- Prolonging the life of your retirement funds by diminishing overall tax obligations.

- Making your yearly tax bill more consistent.

- Preventing the need for substantial withdrawals in later stages of retirement could thrust you into an elevated tax bracket.

By distributing withdrawals over numerous years, it’s possible to lessen the taxable income annually, thereby reducing your exposure to higher taxes.

Bucket Strategy for Withdrawals

The bucket approach will allow you to do smart allocation for retirement. It can help you organize your retirement savings based on when you’ll need them, creating a mix of safety and growth:

- Short-Term Bucket: Holds low-risk, liquid assets for expenses in the next 1-2 years, ensuring you have cash readily available for immediate needs.

- Intermediate-Term Bucket: Contains moderately risky investments for costs expected in the next 3-10 years, balancing growth with some safety.

- Long-Term Bucket: Includes higher-risk investments for expenses more than 10 years out, allowing for greater potential growth over time.

This method gives you a clear plan to manage your money throughout retirement, aligning your investments with your spending timeline.

Advantages and Disadvantages of Bucket Strategies

The bucket strategy provides a mix of detailed control and the opportunity for growth, but it also introduces complexity and requires ongoing time commitment to manage. It enables retirees to use a mental accounting approach that simplifies spending decisions and prioritization.

Yet, this method requires consistent upkeep and realignment, especially within those buckets that contain a larger proportion of equity. Here is where a financial advisor comes in handy!

Timing Your Tax Efficient Withdrawal Strategies

Timing your withdrawals during retirement is crucial for minimizing your tax liability because you can coordinate your withdrawals to spread taxable income across different years. This strategy allows you to take advantage of lower tax brackets during years when your income is lower.

Starting withdrawals before Required Minimum Distributions (RMDs) begin can help you avoid large taxable distributions later on, potentially reducing your overall tax burden.

Don’t forget that withdrawals made before age 59½ typically trigger a 10% penalty and may push you into higher tax brackets. On the other hand, delaying withdrawals until RMDs start can lead to larger taxable amounts and increased taxes.

Also, managing Required Minimum Distributions (RMDs) is essential. These distributions must begin by April 1, following the year you turn 72. Failing to withdraw RMDs on time can result in a significant excise tax penalty.

To maximize your retirement income and minimize tax consequences, strategic planning of withdrawal timing and careful management of RMDs are crucial.

Utilizing Tax-Free Income Sources

By leveraging income streams like Health Savings Accounts(HSAs), municipal bonds, qualified dividends, and social security benefits that offer tax-free advantages during retirement, you can substantially decrease the amount of taxable income you’re responsible for. These strategies are effective in preserving your retirement funds by providing financial efficiencies associated with taxation.

Health Savings Account (HSA)

Health Savings Accounts (HSAs) provide a threefold tax benefit: deductions on contributions, tax-free growth of investments, and the ability to make withdrawals without taxes for qualified medical expenses. They allow you to cover medical and dental costs with the added advantage of indefinite ownership of funds along with tax savings.

Qualified Dividends and Municipal Bonds

On their part, qualified dividends, distributed by either U.S. corporations or eligible foreign entities, are subject to a cap on the federal income tax rate of 20%. Conversely, municipal bonds provide an avenue for earning income that is not subjected to federal income taxes and also escapes state and local taxation.

By incorporating these avenues into your financial strategy, you can decrease your overall liability for federal income taxes. This reduction enhances the manageability of fulfilling your obligation to pay taxes across various jurisdictions.

Planning for Capital Gains

How can capital gains enhance your retirement income? There are mainly two ways:

- Retaining investments over a significant period

- Benefiting from the fact that long-term capital gains are subject to lower tax rates, whereas short-term gains face higher ordinary income tax rates

Such strategic measures aim at minimizing your overall tax liability and optimizing the returns on your investments.

Long-Term vs. Short-Term Capital Gains

Maintaining investments for a period of one year or more allows individuals to benefit from the reduced tax rates applicable to long-term capital gains, in contrast with short-term gains which are subjected to the higher ordinary income tax rates. This variance in how taxes are applied highlights the significance of adopting investment strategies that emphasize holding assets over extended periods as a means to decrease overall tax liability.

Harvesting Capital Gains

Strategically realizing capital gains during years when taxable income is lower allows for the optimization of tax efficiency by leveraging the advantages of lesser tax brackets. This technique dilutes your tax responsibilities over time and prevents accruing enough gains to propel you into a higher tax bracket within any given year, thereby reducing your total taxes owed.

Consulting a Tax Professional

Do you really need to speak to a tax professional?

Yes. Retirees seeking to fine-tune their withdrawal methods to reduce tax responsibilities ought to seek the guidance of a tax professional.

Such experts offer tailored recommendations, pinpoint potential tax benefits, and assist in maneuvering through complex taxation environments. The proficiency of these professionals ensures that your strategy for withdrawals is harmonized with your monetary objectives while also diminishing the total amount you owe in taxes.

Benefits of Professional Advice

Expert guidance can help you formulate a withdrawal plan that minimizes your tax burden as financial advisors and tax experts navigate the intricacies of tax legislation to offer personalized investment counsel aimed at bolstering your retirement earnings. The knowledge they bring is essential for sustaining financial stability over the long haul.

Empowering Financial Futures: The Institute of Financial Wellness (IFW)

The Institute of Financial Wellness (IFW) presents a broad multi-media network that delivers financial education, resources, and services. Engaging in providing e-newsletters, webinars, and on-demand videos full of informative content to its users.

Our Retirement Roadmap service is specially designed to assist those nearing retirement or already retired in realizing their financial aspirations by safeguarding their assets against market fluctuations and undue taxes.

Also, our Retirement Score Webinar, hosted by Erik Sussman, CEO, and Founder of IFW, offers participants a comprehensive strategy to secure their retirement future. Here’s what you can expect:

- Lower or Eliminate Taxes in Retirement: Learn strategies to minimize tax burdens during retirement, ensuring more of your savings stay in your pocket.

- Protect Your Portfolio From Market Volatility: Understand techniques to safeguard your investments against market fluctuations, providing stability in your retirement funds.

- Maximize Retirement Income: Discover methods to optimize your retirement income streams, ensuring financial security throughout your retirement years.

By attending this live webinar, participants will gain personalized insights into assessing their retirement readiness. It promises to equip attendees with actionable tactics to enhance their retirement score and achieve their financial goals effectively.

In pursuit of facilitating the utmost financial prosperity for individuals, IFW’s ensemble of skilled financial experts provides continuous advice and support throughout one’s journey with them.

Full Summary

Maximizing your retirement income through tax-efficient methods involves a strategic approach and thoughtful preparation. It is crucial to grasp the various kinds of retirement accounts available, apply rules such as the 4% guideline, adopt proportional withdrawal tactics and bucket strategies, properly time your distributions from these accounts, and make use of sources providing tax-free income.

Engaging with a tax professional can help fine-tune these approaches, ensuring they are in harmony with your financial aspirations. Through the execution of such strategies, you stand to achieve both security and fiscal stability throughout your retirement years.

Frequently Asked Questions

What are the tax implications of withdrawing from a Traditional IRA?

When you take out money from your Traditional IRA, the withdrawals are subject to ordinary income tax rates. Starting at age 73, you may be required to take minimum distributions (RMDs) from your account.

It’s important to understand these potential consequences on your finances when thinking about withdrawing funds from a Traditional IRA so that you can make decisions that are well-informed.

How many people are retiring in the US?

Since January 2012, retirement has steadily increased, reaching 19.3% in March 2022 [1].

How does a Roth IRA differ from a Traditional IRA in terms of withdrawals?

Withdrawals from a Roth IRA provided the account has been open for a minimum of five years, are not subject to taxes, and there is no obligation for Required Minimum Distributions (RMDs) during the lifetime of the account holder. In contrast, Traditional IRAs mandate RMDs and treat any withdrawals as ordinary income, which is taxable.

How does retirement look like post-pandemic?

As of the third quarter of 2021, 50.3% of U.S. adults aged 55 and older reported being out of the labor force due to retirement.

Before the pandemic (third quarter of 2019), 48.1% of those adults were retired [2].

What are the benefits of the bucket strategy for retirement withdrawals?

The retirement withdrawal bucket strategy segments investments into three categories: short-term, intermediate-term, and long-term buckets. This stratification provides a well-rounded balance between growth potential and financial manageability.

Utilizing this approach can significantly enhance the effective administration of funds during retirement.

How can harvesting capital gains optimize tax efficiency?

Leveraging years when taxable income is lower by harvesting capital gains can utilize the benefit of lower tax brackets to distribute tax liabilities more evenly, which diminishes the total amount owed in taxes.

Such a strategy enhances individuals’ ability to optimize their tax efficiency.

How many people are receiving Social Security benefits?

The number of retired workers receiving Social Security benefits increased from 37.89 million in 2013 to 50.15 million in 2023 [3].

Why is consulting a tax professional important for retirees?

Seeking advice from a tax professional is crucial for retirees to refine their withdrawal methods, reduce their tax burdens, and achieve financial objectives with proficient direction.

This approach paves the way for a more stable and effective retirement financial strategy.

Related Articles

Tax Efficiency in Retirement

Will you pay higher taxes in retirement? It’s possible. But that will largely depend on how you generate income. Will it be from working? Will it be from retirement plans?

Peter Foldes

Nov, 10 2021

What Is a 1035 Exchange?

According to the most recent information available, Americans have individual life insurance with a total face value of $12.4 trillion.1 Due to a variety of factors, these individuals may find

Peter Foldes

Nov, 10 2021

Important Tax Return Deadlines for 2021 Returns

Here is an overview of deadline dates, return types, dates to receive your forms, extensions, etc., and a brief description with helpful tips. Make sure you adhere to the deadlines

Peter Foldes

Dec, 02 2021