“It’s time to enjoy the things you never had time to do when you worked.” -Catherine Pulsifer

What are Boomers, Millennials, and Gen X retirement savings like? Who is saving for their golden years and improving their retirement score?

Each generation faces its own challenges when it comes to achieving a comfortable retirement, but with proper planning and advice from the experts, anyone can enjoy the best lifestyle that they can no matter their age.

Key Takeaways

- Generational Differences in Retirement Planning. Each generation has distinct approaches and challenges when it comes to saving for retirement. Baby Boomers rely on pensions and Social Security, Gen Xers juggle peak earning years with financial obligations, and Millennials leverage technology and start saving early despite economic hurdles.

- Importance of Early and Strategic Saving. Starting to save early and making use of retirement accounts like 401(k)s and IRAs are crucial for building a solid retirement fund. Compound interest and tax-advantaged accounts can significantly enhance savings over time.

- Tailored Financial Planning. Consulting with Certified Financial Planners (CFPs) can help individuals create personalized retirement plans. This is essential for adapting to rising costs and ensuring that various income sources and investments are effectively managed to meet retirement goals.

Retirement Unlocked for Baby Boomers, Gen X, and Millennials

Retirement might seem far away or just around the corner, but understanding it is essential for everyone, no matter your age or savings goals.

However, different generations have different needs and approaches to saving for retirement. So, let’s take a look at the main age groups and how they plan for their future:

- Baby Boomers (born between 1946 and 1964): This group is either already retired or close to it. Many rely on pensions, Social Security benefits, and personal savings. They’ve seen changes in the economy and understand the importance of having a solid retirement plan.

- Generation X (born between 1965 and 1980): Gen Xers are in their peak earning years and are focused on boosting their retirement savings. They balance saving for the future with current expenses, like raising families and paying off mortgages. They often use retirement accounts like 401(k)s and IRAs.

- Millennials (born between 1981 and 1996): Millennials are just starting to think seriously about retirement. They face unique challenges like student debt and rising living costs but also have the advantage of time. Starting to save early means they can benefit from compound interest over many years.

Why Understanding These Differences Is Important

Knowing how each generation approaches retirement helps in planning effectively. For example, Baby Boomers might need to adjust their plans due to rising medical costs or longer life expectancies, while Millennials should start saving now to build a solid nest egg for the future.

Nonetheless, no matter your age, there are some tips you can follow right now so you can retire wealthy and comfortably:

- Start Saving Early: The sooner you start, the more your money can grow thanks to compound interest.

- Use Retirement Accounts: Take advantage of 401(k)s, IRAs, and Roth IRAs to save money in tax-advantaged ways.

- Plan with a Professional: A Certified Financial Planner (CFP) can help you create a personalized retirement plan.

- Consider All Income Sources: Think about Social Security benefits, pensions, and personal savings as parts of your retirement income.

- Adjust for Rising Costs: Plan for inflation and possible increases in living and medical expenses.

- Set Clear Goals: Know how much you need to save to retire comfortably and track your progress.

Retirement Looks Different for Each Generation: What’s Your Plan?

Retirement dreams and goals have changed dramatically over the years. Just as our world has evolved, so have the ways different generations think about their golden years. Let’s dive into how Baby Boomers, Generation X, and Millennials each view retirement and how they’re planning for it.

Baby Boomers: Riding the Wave of Economic Boom

Baby Boomers grew up during a time of economic prosperity following World War II. This era saw rising wages and steady job growth, which shaped how Boomers approach retirement. Many Baby Boomers planned to retire comfortably on a combination of Social Security benefits, pensions, and their own retirement savings.

They often expect to retire earlier and enjoy a leisurely lifestyle.

However, rising inflation and increasing medical costs are pushing some to work longer than expected. Today, many are revisiting their retirement plans and seeking ways to boost their retirement nest eggs.

Certified Financial Planners often recommend strategies like maximizing 401(k) contributions or investing in Roth IRAs to ensure a stable retirement income.

Generation X: Navigating Economic Shifts and Technological Growth

Generation X witnessed significant economic changes and the rise of technology. They experienced the dot-com bubble, the financial crisis of 2008, and the transformative power of the internet. These events have led Gen X to approach retirement planning with a mix of caution and adaptability.

Unlike Boomers, many Gen Xers may not have pensions and must rely more on their own savings. The average retirement savings for this group varies widely, with many still trying to catch up after years of financial ups and downs.

Financial experts often stress the importance of starting to save for retirement early and making use of retirement savings plans like 401(k)s and IRAs. With the average savings often not enough to retire comfortably, Gen Xers are keen on finding ways to stretch their retirement dollars and may even consider working past the traditional retirement age.

Millennials: Shaping Retirement in the Digital Age

Millennials are the first generation to grow up in the digital age. They have faced unique challenges like student loan debt and the Great Recession, which have impacted their views on retirement.

Despite these hurdles, Millennials are known for their forward-thinking and adaptability.

They’re more likely to invest in the stock market and are often savvy about using technology to manage their finances. Many Millennials are starting to save for retirement earlier than previous generations, recognizing the power of compound interest.

Retirement planning for them often includes a mix of traditional retirement accounts and innovative financial strategies. While many Millennials worry about the future of Social Security benefits, they are also exploring ways to generate extra money and invest wisely to secure their financial future.

A Changing Landscape for All

Across all these generations, one thing is clear: Retirement planning is crucial. Whether it’s maximizing savings rates, understanding the benefits of different retirement accounts, or adjusting to living expenses and medical costs, planning ahead can make a big difference.

The National Council on Aging and other organizations provide valuable resources to help individuals navigate their retirement planning. No matter your age group, starting early and seeking advice from financial professionals can help you set achievable retirement savings goals and build a comfortable future.

Will Gen X Make It to a Comfortable Retirement? What Are Gen X Retirement Savings Like?

Let’s look at some data. Only 40% of Gen X workers think they’ll save enough to retire comfortably.

In fact, many Gen Xers are worried about their finances. About 69% feel they’re not saving enough, and almost half believe they’re way behind [1].

There’s a big gap between what they have now and what they need for a secure retirement.

Average Retirement Savings for Gen X

The average retirement savings for Gen X is about $313,220. However, this figure can be misleading as it includes the savings of high earners.

For those aged 55-64, the average savings jumps to $537,560. But when we look at typical households, the picture is less rosy, with many Gen Xers having significantly lower savings.

A typical Gen X household has about $40,000 in retirement savings, far below the average of $153,300. This discrepancy highlights the uneven distribution of retirement funds among Gen Xers.

Despite these sobering figures, Gen X has shown an average savings rate of 15.2% of their annual pay, which is slightly above the recommended 15% [2]. This indicates that while some Gen Xers are saving diligently, the overall savings figures are skewed by those who are not saving enough.

Moreover, Gen X is the first generation to primarily use 401(k) plans instead of traditional pensions, which requires more proactive management of their retirement funds.

Comparison to Other Generations

When comparing the retirement savings of Gen X to other generations, significant disparities emerge. Older generations, particularly Baby Boomers, tend to have higher average transaction account balances due to more favorable economic conditions and more common pension plans.

For instance, those aged 65-74 have an average transaction balance of $60,410, compared to $48,200 for Gen Xers aged 45-54.

This comparison underscores the unique challenges faced by Gen X in accumulating sufficient retirement savings.

Challenges Facing Gen X in Saving for Retirement

Gen X faces several unique challenges in saving for retirement, making it harder for them to accumulate a sufficient retirement nest egg. Some of these challenges include:

- Nearly half of Gen Xers worry they won’t have enough money for retirement

- 31% fear they’ll never save enough to retire

- The financial stress of supporting both elderly parents and adult children, often referred to as the “sandwich generation”

Economic Factors

Economic factors such as inflation and wage stagnation have significantly impacted Gen X’s ability to save for retirement. Some key factors include:

- Over 54% of Americans have stopped or reduced their retirement savings due to inflation.

- Gen X has lived through multiple economic crises, which have affected their ability to save.

- Wages have not kept up with inflation, making it challenging for Gen X to save adequately.

These factors have made it difficult for Gen X to save enough for a comfortable retirement.

Rising costs are a significant concern, with almost two-thirds of Gen Xers saving less due to higher everyday costs.

Employment Stability

Employment stability is another major concern for Gen X. About 30% worry they won’t be able to work as long as they would like, and 46% are concerned they may have to return to work after retirement due to financial needs.

These fears are exacerbated by the mental and emotional health challenges linked to financial insecurity and retirement planning. Keeping an eye on labor statistics can help individuals better understand the job market and make informed decisions about their careers.

Healthcare and Medical Costs

Healthcare and medical costs are significant hurdles for Gen X. Over a third of Gen Xers worry that healthcare costs will deplete their retirement savings.

Typical healthcare costs in retirement for a couple are around $315,000, and long-term care costs can exceed $100,000 annually. These expenses underscore the importance of having a robust financial plan that incorporates healthcare costs.

Strategies for Boosting Gen X Retirement Savings

To address these challenges, Gen X needs to adopt effective strategies to boost their retirement savings. Consistently contributing to retirement accounts, such as IRAs and 401(k)s, and seeking professional financial advice are critical steps.

Maximizing 401(k) Contributions

Maximizing 401(k) contributions is a powerful strategy for Gen X to enhance their retirement savings. By leveraging their peak earning years, Gen Xers can significantly boost their retirement funds.

Gradually increasing contributions by 1% of annual salary and setting up automatic increases when receiving raises can make a substantial difference.

Additionally, taking full advantage of employer matching contributions can effectively double one’s savings.

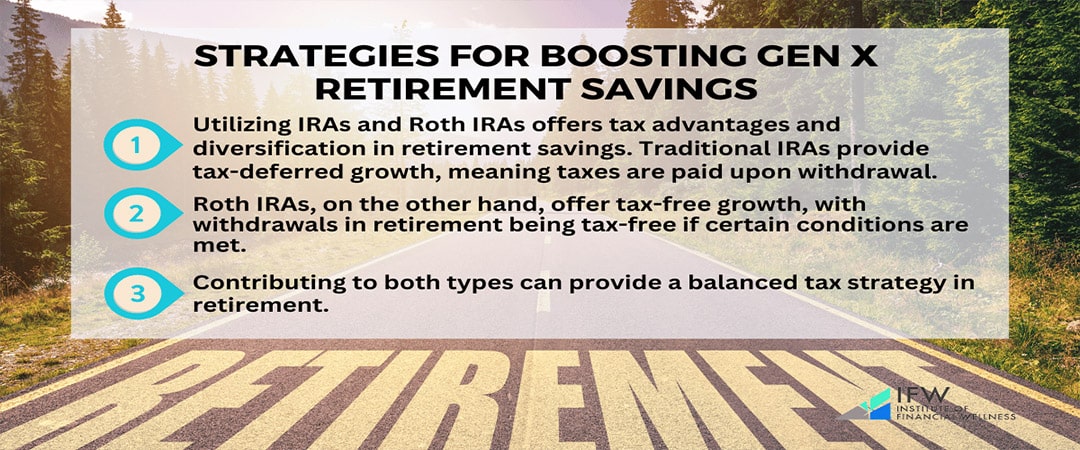

Utilizing IRAs and Roth IRAs

Utilizing IRAs and Roth IRAs offers tax advantages and diversification in retirement savings. Traditional IRAs provide tax-deferred growth, meaning taxes are paid upon withdrawal.

Roth IRAs, on the other hand, offer tax-free growth, with withdrawals in retirement being tax-free if certain conditions are met.

Contributing to both types can provide a balanced tax strategy in retirement.

Financial Planning with a Certified Financial Planner

Consulting with a certified financial planner (CFP) can help Gen Xers create personalized retirement plans tailored to their financial goals. Many Gen Xers are realizing the importance of professional advice when navigating their retirement plan.

A CFP can provide insights on optimizing investment strategies and managing expenses, ensuring that savings grow steadily over time.

Empowering Financial Futures: Comprehensive Education and Resources by the Institute of Financial Wellness (IFW)

The Institute of Financial Wellness (IFW) offers a comprehensive array of financial education, resources, and services to help individuals make informed financial decisions. The IFW provides engaging, informative, and objective financial education content, including e-newsletters, webinars, video-on-demand (such as The Retirement Score Webinar), and the IFW Retirement Roadmap.

The Retirement Roadmap empowers individuals to achieve their retirement dreams by eliminating the fear of running out of money and protecting retirement assets from market volatility and unnecessary taxation.

The IFW also offers financial check-ups, which help individuals ensure their financial health is on track for sustainable well-being. By providing clarity and confidence, the IFW helps individuals make informed decisions and take action to secure their financial future.

The IFW’s network of financial professionals is committed to a holistic and unbiased approach, ensuring that every financial decision is tailored to the individual’s unique needs.

Full Summary

Retirement planning is a critical aspect of financial well-being, no matter your age or current savings. Baby Boomers, Generation X, and Millennials each have unique perspectives and strategies for approaching their golden years.

Understanding these generational differences highlights the importance of starting to save early, utilizing retirement accounts, and seeking professional advice. Across all generations, setting clear goals and adjusting for rising living and medical costs are essential steps in creating a robust retirement plan.

Frequently Asked Questions

What is the average retirement savings for Gen X?

The average retirement savings for Gen X is about $313,220 but can vary depending on individual circumstances. It’s important to consider personal financial goals and resources when planning for retirement.

How many Baby Boomers have retired in the last years?

From 2012 to the third quarter of 2020, a total of 28.6 million Baby Boomers have retired in the United States [3].

Why is it important for Gen X to not rely solely on Social Security?

It’s important for Gen X to not rely solely on Social Security because there is uncertainty about its reliability and whether it will be enough to cover living expenses in retirement. This uncertainty makes it risky to depend only on Social Security.

What are some strategies for Gen X to boost their retirement savings?

To boost their retirement savings, Gen X can maximize 401(k) contributions, utilize IRAs and Roth IRAs, and consult with certified financial planners for personalized retirement plans. These strategies can help them secure a comfortable retirement.

How can Gen X calculate their future living expenses for retirement?

To calculate future living expenses for retirement, Gen X should consider their desired lifestyle, daily living costs, healthcare expenses, and tax rates in retirement. These factors will help them estimate their financial needs accurately.

What resources does the Institute of Financial Wellness offer?

The Institute of Financial Wellness offers a range of resources, including financial education content, webinars, video-on-demand, the IFW Retirement Roadmap, and the Financial Check-up, among others. These resources can help individuals improve their financial well-being and plan for retirement.

Related Articles

The Stages of Financial Life

As we transition through the various stages of life, our financial needs are also constantly evolving. The Institute of Financial Wellness examines the various stages of financial life and the

Evan Sussman

Oct, 25 2021

Traditional IRA vs. Roth IRA

Traditional Individual Retirement Accounts (IRA), which were created in 1974, are owned by roughly 36.1 million U.S. households. And Roth IRAs, created as part of the Taxpayer Relief Act in

Peter Foldes

Nov, 10 2021

Tax Efficiency in Retirement

Will you pay higher taxes in retirement? It’s possible. But that will largely depend on how you generate income. Will it be from working? Will it be from retirement plans?

Peter Foldes

Nov, 10 2021