“Wealth is the ability to truly experience life. Being rich isn’t about owning things; it’s about being able to do things and enjoy experiences.” -Jim Rohn

“How much cash should I have on hand before I retire?” We know that is a question you may be asking yourself, along with “What is my Retirement Score?” and “How can I maintain a fun lifestyle during retirement?”

Experts typically recommend maintaining between 2% to 10% of your portfolio as cash when considering retirement. So, let’s dive right into it and determine the amount of cash you should keep readily available by examining your personal financial objectives, establishing an emergency fund, and assessing your regular monthly expenditures.

Key Takeaways

- Financial security + growth. Experts recommend holding 2% to 10% of your retirement portfolio in cash to cover living expenses and emergencies, ensuring financial security without compromising investment growth.

- Use accounts with high interest rates. High-yield savings accounts and money market accounts are preferred options for storing cash reserves due to their higher interest rates, accessibility, and safety features.

- Have reserves for emergencies. Maintaining cash reserves equivalent to one to two years of living expenses during retirement helps manage economic uncertainties, avoiding the need to liquidate investments at a loss during market downturns.

Determining Your Cash Reserve Needs in Retirement

Thinking about how much cash to keep when you retire? It can feel tricky.

The answer depends on your age, savings, and lifestyle plans. You need enough money to cover your daily expenses and any surprises without missing out on the growth of your retirement funds.

Experts suggest keeping about 2% to 10% of your investments in cash. This balance protects you without slowing down the growth of your other assets.

Here’s how to plan your cash reserve:

- Check Your Monthly Spending: Know how much you spend each month.

- Set Up an Emergency Fund: Have money ready for unexpected costs. Tailor it to your financial goals.

- Personal Factors: Consider your unique situation and financial needs.

It’s essential to review and adjust your plan regularly. This way, you can be prepared for both unexpected events and changes in your life.

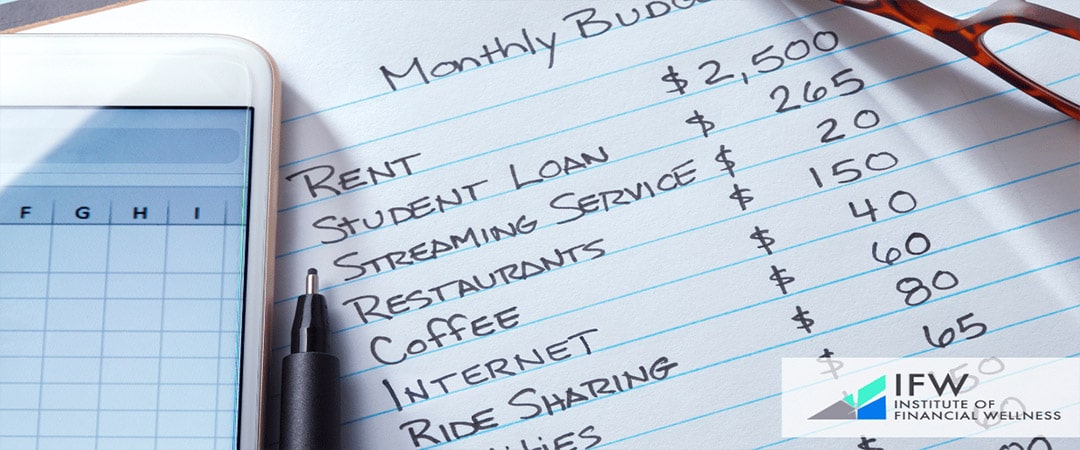

Evaluating Monthly Expenses

To figure out how much cash you need in retirement, start by looking at your expected monthly expenses. Break these down into two categories:

- Fixed Costs: These are things like housing, utilities, and insurance. They usually make up about half of your budget.

- Variable Costs: These include food, fuel, and entertainment. For most Americans, these costs add up to just under $1,000 per month.

Knowing your monthly spending helps you understand how much cash you’ll need to cover your basic needs without dipping into your long-term investments.

It’s also smart to keep some cash handy for emergencies. This gives you a cushion to handle unexpected expenses, like car repairs or medical bills, without having to sell investments.

By planning for both your regular monthly expenses and a small emergency fund, you can stay prepared and protect your financial future.

Considering Emergency Fund Size

Emergencies: How much is enough?

When planning for retirement, it’s crucial to have an emergency fund. Most financial experts recommend saving enough to cover three to six months of your expenses.

This helps you manage unexpected costs without touching your retirement savings.

An emergency fund is your safety net. It keeps you from having to sell investments when the market is down.

By having cash set aside, your long-term investments can keep growing without interruption.

Some financial experts, like Suze Orman, suggest saving even more—enough to cover up to eight months of expenses. This extra cushion offers greater security and peace of mind, especially during tough times.

Here’s how you can set up your emergency fund:

- Calculate Your Monthly Expenses: Add up your regular costs, like rent, utilities, groceries, and transportation.

- Multiply by 3-6 (or more): Based on expert advice, decide how many months of expenses you want to cover. Multiply your monthly expenses by this number.

- Start Saving: Begin setting aside this amount in an easily accessible account, separate from your long-term investments.

Having a robust emergency fund is a key part of a solid retirement plan. It protects you from financial surprises and keeps your investments growing.

Accounting for Personal Financial Goals

How much cash should you keep for retirement? It all depends on your unique financial goals and needs.

Regularly reviewing your cash reserves is essential. As your life changes, like receiving an inheritance or a big bonus, you may need to adjust how much cash you keep.

This ensures your reserves stay in line with your overall investment strategy.

Your personal risk tolerance is a key factor. Think about how much risk you’re comfortable with and how much financial uncertainty you can handle.

Your spending and saving habits also play a big role. Understanding your habits helps determine the right amount of cash to keep on hand.

Long-term goals are another crucial consideration. Reflect on what you want to achieve in the future; your cash reserves should support these goals without putting your investments at risk.

Finding the right balance is important. Keep enough cash to feel secure and handle emergencies, but not so much that it limits the growth of your investments.

By regularly reviewing and adjusting your cash reserves, you can manage risks and stay aligned with your financial goals. This approach ensures your cash strategy supports your overall financial health and helps you enjoy a comfortable retirement.

Where to Keep Your Cash Reserves

Once you know how much cash you need for retirement, the next step is deciding where to keep it. There are several good options, each with its own benefits for security, accessibility, and earning potential. Let’s look at some popular choices:

- High-Yield Savings Accounts: These accounts are great for keeping your cash safe while earning interest. They usually offer higher interest rates than regular savings accounts. Your money is easy to access, and these accounts are typically insured by the FDIC, so your funds are protected.

- Money Market Accounts: Money market accounts combine features of both savings and checking accounts. They often come with higher interest rates and some check-writing privileges. Like high-yield savings accounts, they are usually FDIC-insured, providing a safe place to keep your cash.

- Checking Accounts: While they generally offer lower interest rates, checking accounts provide the most flexibility for accessing your money. You can write checks, use a debit card, and make quick transfers, making them ideal for everyday expenses and emergencies.

Finding the Right Mix

Choosing the right places to keep your cash is crucial. You want to secure your funds while also taking advantage of any interest-earning opportunities.

Think about your needs for accessibility and the balance between earning interest and having your money readily available.

By selecting suitable accounts for your cash reserve, you can protect your funds and potentially earn some interest. This approach fits into a larger strategy for managing your cash reserves, ensuring your financial stability, and supporting a comfortable retirement.

We will explore these options further to see how they fit into a broader plan for managing your cash effectively.

Balancing Cash with Investments During Retirement

Ensuring the right mix of cash, cash equivalents, and investments is crucial for financial health during retirement. The role of cash within an investment portfolio includes:

- Providing liquidity

- Stabilizing the portfolio

- Serving as a reserve for emergencies

- Creating opportunities to invest

Possessing excessive amounts of cash can have varying advantages and drawbacks depending on one’s unique situation.

With interest rates shifting, there are new opportunities to improve your investment results by allocating portions of your available cash into short-duration instruments with higher yields. It’s wise to conduct periodic evaluations of the allocation dedicated to cash in your investment strategy.

This should be done yearly or even more often if changes occur in your circumstances.

A well-rounded investment portfolio tailored for both immediate needs and future objectives typically encompasses an assortment that spans stocks, bonds, and some amount of liquid assets like money market funds. In our analysis ahead, we’ll delve into strategies for finding equilibrium between these essential components effectively.

Risk Tolerance and Market Volatility

Recognizing your level of comfort with investment risk is vital to safeguard against potential losses that can occur during periods of volatility in the stock market. During uncertain times in the market, it may be necessary to modify your cash reserves as a precautionary measure to maintain financial stability until there is a recovery in the market.

Your decision-making regarding certain financial matters could be influenced by fluctuations within the market, including:

- determining an appropriate amount of accessible cash

- deciding when it’s best to liquidate assets into cash

- considering how long you should retain assets in their cash form

- making significant optional expenditures

To ensure that your investment approach remains attuned both to changing needs and tolerance for risk, regular evaluations and updates are critical.

Short-Term Investments

Investments that are conservative and liquid, such as cash or money market accounts, should make up the short-term segments of your investment portfolio, covering a time frame of one to three years. Ensuring your portfolio includes cash equivalents can protect against declines in the market while keeping funds readily available.

Having these kinds of short-term investments is essential for providing the liquidity required to meet immediate financial demands without having to liquidate long-term investments at an unfavorable loss. They are instrumental in preserving economic security throughout retirement.

Cash Equivalents in Your Portfolio

Looking to add some stability to your investments? Cash equivalents might be just what you need! These include safe options like certificates of deposit (CDs), Treasury bills, and municipal bonds.

- Certificates of Deposit (CDs): CDs are insured by the FDIC, making them a safe place for your money. You agree to leave your funds in for a set period, and in return, you get a guaranteed interest rate.

- Treasury Bills (T-bills): Backed by the U.S. government, T-bills are one of the safest investments out there. They offer easy access to your money (liquidity) and provide modest returns.

- Municipal Bonds (Munis): These bonds are supported by state or local governments. They offer reliable income and a safe place to park your cash.

Incorporating these cash equivalents into your portfolio can enhance its stability and provide a steady stream of income.

How Much Cash Should I Have on Hand as a Reserve for Life Changes

Life can throw unexpected expenses your way during major milestones like changing jobs, getting married or divorced, or receiving unexpected windfalls. These events often require a reassessment of your financial situation to cover new or unforeseen costs.

One effective strategy is to regularly rebalance your portfolio, especially after significant life changes or on an annual basis. This ensures that your cash reserves are aligned with your evolving financial needs.

Let’s delve into specific strategies for adjusting your cash reserves during these pivotal life transitions.

Job Changes and Career Transitions

When undergoing career changes, it is prudent to build up additional cash reserves. This strategy assists in bridging any income disruptions or covering elevated expenses during the transition from one job to another.

Having a more substantial financial cushion can be critical when facing relocation costs or necessary training fees associated with changing careers. Ensuring you have adequate cash on hand helps facilitate a stress-free shift between professional endeavors by preparing for these foreseeable expenditures.

Marital Status Changes

Altering your marital status can have a considerable effect on the need for cash reserves because of the expenses that come with either marriage or divorce. Divorce may lead to substantial financial demands, such as legal costs, splitting assets, and setting up individual homes, which could strain your current financial situation.

It’s vital to re-evaluate and adapt your cash reserve accordingly to prepare for these possible outlays and maintain fiscal health.

Likewise, when getting married, it’s important to modify cash reserves in response to new combined household expenditures and possibly shared economic objectives. Taking the initiative to adjust your financial plans for changes in matrimonial status is key to promoting monetary security during these significant periods of change.

Major Purchases and Windfalls

To prepare for significant expenditures such as acquiring a new home or vehicle, it’s crucial to bolster your cash reserve. This step is necessary to cover upfront payments and related expenses, securing ample liquidity while safeguarding your overarching financial objectives.

In the event that you come into unexpected wealth – whether from an inheritance or substantial bonus – revisiting your plan for maintaining a cash reserve becomes vital. Engage with a financial consultant to examine investment opportunities in harmony with the existing cash within your portfolio, thereby enhancing the overall strategy of your finances and investments.

Maintaining Cash Reserves During Retirement

Planning for retirement involves ensuring you always have enough cash on hand. This flexibility allows quick access to funds and protects against market downturns.

Experts recommend keeping aside one to two years’ worth of living expenses in these reserves. This buffer helps manage economic shifts or unexpected expenses without needing to sell investments prematurely.

One effective strategy is the Bucket Strategy, which categorizes your resources into short-term, medium-term, and long-term allocations. This approach ensures you have enough conservative investments readily available, reducing the need to sell assets when market values are low.

Avoid hoarding excessive cash in banks, as it may yield lower returns compared to investing. Instead, strike a balance by keeping enough cash while also investing to grow your wealth.

This balanced approach helps maintain and potentially increase your financial security while minimizing unnecessary risks and losses.

Social Security and Other Income Sources

Social Security offers a reliable source of income, diminishing the necessity to maintain substantial cash reserves. This reliable benefit stream can serve as an economic safeguard, enabling individuals to keep less in emergency funds.

Other forms of steady income such as pensions, earnings from rental properties and supplemental part-time employment contribute to one’s financial solidity. These varied streams of revenue have the effect of potentially reducing the requirement for large cash reserves by bolstering overall financial security.

Empowering Financial Mastery: The Institute of Financial Wellness (IFW)

The Institute of Financial Wellness (IFW) stands as a diverse multi-media hub dedicated to providing educational content, resources, and services in finance. Our core objective is empowering people to excel financially and live enriching lives by providing engaging, factual financial education.

IFW offers a variety of tools, such as complimentary e-newsletters, webinars accessible both live and on-demand, and video material covering crucial subjects like retirement preparation strategies and investment approaches, such as the Retirement Score Webinar. These offerings aim to bestow clarity upon users so that they can execute financial decisions with greater certainty.

By participating with the IFW, you gain:

- Entry into a network populated by seasoned experts in finance

- Tailored counsel along with solutions designed for each person’s unique financial circumstance

- A comprehensive strategy intended to enhance every facet of an individual’s fiscal health

- The agency needed for individuals desiring mastery over their economic destiny

Full Summary

Calculating how much cash to retain before stepping into retirement should be based on an evaluation of your regular expenses and emergency fund needs while aligning with your individual financial aspirations. It’s advisable to allocate about 2-10% of your investment portfolio in cash reserves for both fiscal security and adaptability.

Positioning your monetary reserves across high-yield savings accounts, money market accounts, and checking accounts ensures that you benefit from safety, easy access, and some interest income growth. Achieving a healthy equilibrium between liquid assets (cash) and investments is key. This involves accounting for personal risk tolerance levels along with considerations about market volatility and the immediate need for funds within short-term horizons.

It’s imperative to modify one’s reserve strategy when encountering major life transitions while also effectively managing these resources throughout retirement years. Implementing approaches such as the Bucket Strategy alongside utilizing sources like Social Security benefits can aid in navigating through these changes efficiently.

By adhering to such advice detailed above, crafting a thoughtful cash reserve blueprint becomes achievable – one which resonates with specific financial targets tied deeply to one’s unique circumstances thus bolstered preparedness for a stable & rewarding post-retirement phase ensues.

Frequently Asked Questions

How much cash should I have on hand before retirement?

Your individual financial situation should be a primary consideration. Factors including age, lifestyle choices, and the cost of your regular monthly outgoings all play a part in determining this.

Financial experts suggest maintaining an amount that ranges from 2% to 10% of your investment portfolio as liquid savings or cash.

What are emergency saving trends in the US?

27% of U.S. adults have no emergency savings at all, which is the highest percentage since 2020 [1].

What are the best places to keep my cash reserves?

For your cash reserves, you might want to consider utilizing checking accounts, money market accounts, and high-yield savings options. They offer the advantage of keeping your money secure and easily accessible while also affording you the possibility of earning interest.

How do I balance cash with investments during retirement?

During retirement, it’s essential to strike a harmony between cash holdings and investments by taking into account your appetite for risk, the fluctuations of the market, and commitments in short-term investments. Continuous monitoring of your portfolio is crucial to maintain alignment with your financial objectives despite market volatility.

How much money have Americans saved up?

As of April 2023, total U.S. personal savings amounted to $802.1 billion.

The personal savings rate, which represents personal savings as a percentage of disposable personal income, stood at 4.1%.

Excluding retirement assets, the average American has approximately $65,100 in personal savings [2].

How should I adjust my cash reserves for life changes?

You should adjust your cash reserves for significant life events like job changes, marital status changes, and windfalls to ensure you’re prepared for new financial demands.

How much money do millionaires have in savings?

The top 1% of American households have about $2.5 million in savings [3].

How can I maintain cash reserves during retirement?

To preserve your cash reserves throughout retirement, it’s advisable to implement the Bucket Strategy. This involves setting aside short-term funds specifically for periods when the market is down, thereby safeguarding your finances.

You can bolster your income by tapping into other resources like Social Security.

Employing these tactics will contribute to sustaining a secure financial footing during your retirement years.

Related Articles

The Stages of Financial Life

As we transition through the various stages of life, our financial needs are also constantly evolving. The Institute of Financial Wellness examines the various stages of financial life and the

Evan Sussman

Oct, 25 2021

Traditional IRA vs. Roth IRA

Traditional Individual Retirement Accounts (IRA), which were created in 1974, are owned by roughly 36.1 million U.S. households. And Roth IRAs, created as part of the Taxpayer Relief Act in

Peter Foldes

Nov, 10 2021

Tax Efficiency in Retirement

Will you pay higher taxes in retirement? It’s possible. But that will largely depend on how you generate income. Will it be from working? Will it be from retirement plans?

Peter Foldes

Nov, 10 2021