Do you want to optimize your retirement savings and enjoy tax-free golden years? Look no further than our all-inclusive “Retirement Ready Checklist”. Let’s share some insights with you on how to diversify investments as well as pick the perfect destination for living out those cherished retirement dreams with minimal taxes! Just follow this comprehensive guide, and it will put you firmly on the path toward fulfilling your long-awaited goal of retiring comfortably.

Key Takeaways

- Assess, diversify, and rebalance retirement savings for optimal returns.

- Maximize contributions to employer-sponsored plans, IRAs, and Roth IRAs.

- Calculate income needs, develop a withdrawal strategy, plan for healthcare expenses, and determine the ideal lifestyle/location.

Assess Your Retirement Savings and Investments: Retirement Checklist

Having a successful retirement requires staying on top of your savings and investments. To create the life you want, diversifying wisely and regularly rebalancing is essential for this financial goal. Reviewing what’s in your portfolio consistently will help keep it balanced while securing a secure future post-career day. Managing these assets correctly should give you more confidence to enjoy all that comes with spending those golden years comfortably retired!

Diversify your portfolio

When saving for retirement, having a balanced portfolio of different stocks and bonds can help increase returns while minimizing risk. It’s advisable to not allocate more than 10-20% of the total savings into employer stock. There are also potential tax advantages from rolling over company shares held in an IRA. Exploring strategies around net unrealized appreciation could be beneficial.

Rebalance investments regularly

Periodically reassessing your investments helps keep the desired asset allocation consistent and adaptable to market shifts, thus decreasing risks while amplifying returns. To get successful results from rebalancing, have a set timeline for it. Put tax-efficient strategies into effect so as to avoid taxes. Assess the costs involved in order that they match up with your financial objectives.

Maximize Retirement Account Contributions

Retirement security can be achieved by taking full advantage of employer-sponsored plans, traditional IRAs, and Roth IRAs when it comes to maximizing your contributions. Make sure you maximize what goes into health savings accounts, too – these are an invaluable resource for building up retirement wealth over time. By making wise investments in saving opportunities such as the ones mentioned above, retirees will have a much more secure financial situation during their golden years than they would otherwise.

Employer-sponsored plans

When planning for retirement, it is important to take full advantage of employer-sponsored plans such as 401(k)s and 403(b)s by contributing whatever possible. Your employer may even offer matching contributions, so don’t miss out on these potential benefits! Contribution limits are up to $19,500 in 2020 with an extra catchup contribution allowance of $6,500 if you’re aged 50 or over – make sure you are aware of this cap when making your financial decisions.

IRAs and Roth IRAs

Retirement savings are important, and both Traditional IRA and Roth IRAs can help you achieve that. Contributions to a traditional IRA qualify for tax deductions, while earnings on investments in a Roth IRA are exempt from taxation when withdrawn at retirement. For individuals aged 50 or above, the contribution limit per year is $7,000. Otherwise, it’s set as $6,000 yearly across all types of IRAs/Roth IRAs. To get started with either kind of account, just visit your local bank institution, where they will need some personal details about yourself!

Calculate Your Retirement Income Needs

When it comes to retirement, one must accurately assess their income needs in order for a comfortable lifestyle. Thinking of Social Security benefits, pensions, and annuities can be essential components when calculating your financial future.

Social Security benefits

Retirement income often depends on strategic planning, and one of the methods for achieving that goal is spending from your retirement savings before receiving Social Security benefits. It can help sustain financial stability in later years.

The official full retirement age lies between 66 to 67, but you may start obtaining Social Security retirement rewards anytime between 62-70 years old. If they wait until after reaching the maximum retirement period, then they will receive an 8% raise per year up to 70 years old, which adds extra motivation as a great incentive.

Pension and annuities

Pensions and annuities can be advantageous for those looking to create a source of income during their retirement years. An SPIA is an excellent option as it provides financial benefits in the form of regular payments, with just one premium payment upfront. Consider different types of annuities when deciding which will provide you with the best solution tailored to your personal finances.

Develop a Withdrawal Strategy

To properly manage retirement assets and ensure current income requirements are met, a strategic withdrawal plan should be created that takes into account the timeline to reach your retirement date. Tax-efficient withdrawals will also help maintain sustainable withdrawal rates over time. This planned approach towards withdrawing from savings is essential in making sure you receive enough funds during your years of nonworking while protecting any remaining funds for use throughout the rest of one’s retired life.

Tax-efficient withdrawals

When it comes to retirement accounts, strategizing for tax-efficient withdrawals is the way to go if you wish to get maximum income with minimal taxes. As RMDs start at 70 1/2 years of age, remember your target date so that you are well prepared ahead of time. If your current tax bracket happens to be low, then think about converting traditional IRAs into Roths. This will help guarantee some form of taxation-free income once in retirement.

Sustainable withdrawal rate

Determining a withdrawal strategy that maintains your retirement savings while allowing for necessary income is key to ensuring its longevity. A sustainable withdrawal rate allows you the annual percentage of funds from these investments with minimal risk of exhausting them during the course of your retirement life. It’s essential to provide current financial needs without depleting resources allocated for later use.

Plan for Healthcare Expenses

Retirees have to consider healthcare expenses as a key concern, and planning ahead for long-term care as well as being informed about Medicare options are two effective strategies that can help safeguard retirement savings while also providing medical support.

Medicare options

Research the different Medicare options, like Parts A, B, and D, that take care of hospital expenses, medical practitioner services as well as a portion of prescribed drugs. Examine your particular coverage in-depth – including premiums/deductibles/copayments, etc, and items not included in order to prepare for sound healthcare protection during retirement. Evaluate out-of-pocket charges so you are financially prepared when the time comes!

Long-term care planning

When planning for long-term care expenses, it is important to consider insurance options that will help protect your retirement savings. Long-term care coverage offers financial support for a variety of services, such as home health assistance, assisted living, and nursing homes.

Evaluate all needs both now and in the future. Look into what type of extended care can be provided along with different financing solutions so you are ready if any potential costs arise from long-term healthcare plans.

Determine Your Ideal Retirement Lifestyle and Location

Your retirement experience can be greatly impacted by the sort of lifestyle and location that you aim for. Downsizing, shifting residences, or investigating active adult neighborhoods may help to find what best fits your planned retirement goals. These options could aid with reducing costs while still experiencing a more relaxed atmosphere and discovering a community suited specifically to you.

Downsizing or relocating

When planning for retirement, relocating to a more cost-effective area or downsizing can potentially improve your lifestyle. Be sure to take into consideration the local housing market, amenities offered in that region, the potential tax implications, and how close you’ll be able to stay with family and friends when examining different options.

Active Adult Communities

For retirees, active adult communities offer enhanced safety and security with low-maintenance living arrangements. These communities also provide economic advantages such as reduced property taxes, along with resort-style amenities that promote an activity and fitness-oriented lifestyle. Prime locations make it easy to create a sense of community amongst residents who are looking for minimal upkeep coupled with the perfect retirement experience.

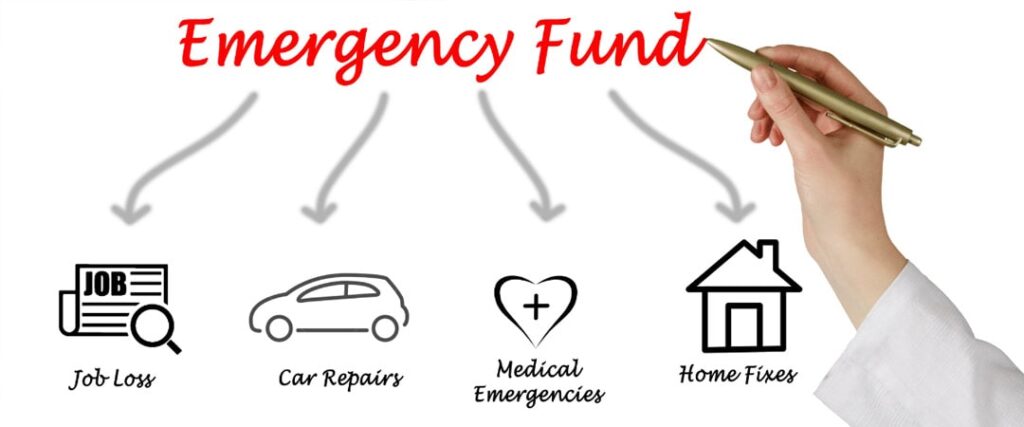

Eliminate Debt and Create an Emergency Fund

For a secure financial future during retirement, debt should be eliminated, and an emergency fund established. Having adequate cash flow to meet retirement costs is essential in order for one’s retirement funds to effectively carry them through the golden years. To achieve these goals, it’s important to create a plan of action that includes paying off debts and stashing away savings specifically meant for emergencies or unexpected events. By doing so, you will ensure your hard-earned money continues working even when you retire!

Debt repayment strategy

For those facing financial challenges during retirement, a debt repayment strategy could help reduce high-interest debts and lighten the burden. One way to begin is by increasing mortgage payments while refraining from adding any more credit card debt. Another option would be deciding between paying off the smallest balance or tackling what has been charged with a higher interest rate first. Whatever approach one takes, it should greatly benefit their overall stress levels when managing finances in later life stages.

Building an emergency fund

It is important to have an emergency fund of at least six months’ worth of expenses in order to protect your retirement savings from being used up unexpectedly. Place it somewhere safe and separate from other funds. Such as a passbook savings or money market account. You can set up automatic transfers so that every paycheck goes towards the emergency fund, cut back on nonessential spending, and consider working extra hours for extra cash, all helping you create this crucial safeguard against future calamities.

Consult with a Financial Advisor

When it comes to retirement planning, engaging the support and counsel of a financial advisor is key to achieving success. This type of professional guidance ensures well-informed decisions are made regarding your pension plan, as well as gaining access to income tax advantages. As you navigate through this stage in life, obtaining personalized advice and continuing assistance from an expert can make all the difference with regard to preserving your wealth, assets, and income over time.

Choosing the right advisor

When it comes to selecting a financial advisor, consider the individual’s credentials and background. Ask for referrals from trusted sources such as family members or acquaintances. Also, look into online reviews and then have an interview with potential advisors in order to make sure they fit your needs and goals. Taking these steps can ensure you find the most suitable professional for you.

Ongoing financial guidance

Your financial advisor can be your guide throughout your retirement journey, providing ongoing advice and support to ensure that you stay on track with achieving your goals. They have the expertise needed for monitoring investments while taking into consideration any alterations in both life circumstances or the market conditions affecting a tailored-made plan specifically designed around individual needs.

By keeping an open dialogue between client and adviser, they are able to make sure all decisions made offer peace of mind due to being backed by sound knowledge, which allows them to serve as dependable sources capable of aiding those looking forward towards their future financially.

The Institute of Financial Wellness Can Help You if You’re Getting Ready to Retire

The Institute of Financial Wellness is there to aid you with planning for retirement so that when the time comes, your golden years will be enjoyed in a tax-efficient way. They are able to put together a plan based on where you currently stand financially and deliver it using an efficient checklist system, too.

This means your efforts towards preparing for retirement can yield all kinds of positive results: from achieving those dreams of yours easily up until confidently embracing your future financial situation without any worries whatsoever!

Full Summary

It is necessary to properly prepare for retirement in order to maximize your income and have a tax-efficient plan. Planning should involve diversifying investments, contributing as much as possible to any relevant accounts, determining estimated costs of living during this period, and setting up an effective withdrawal strategy that will be beneficial in the long run. Take care of health expenses, including insurance or other means, beforehand, alongside deciding on where you wish to live out these years by contemplating lifestyle choices, deliberating over debt issues that could occur if not managed priorly, and speaking with a financial advisor who can offer guidance accordingly. With all this taken care of correctly, one stands well poised to enjoy their post-work life comfortably!

Frequently Asked Questions

What is the first thing to do before retiring?

Prior to retiring, having a full understanding of your financial situation is essential. This entails taking inventory of all assets you have and scrutinizing any sources from which income derives while factoring in Social Security payments, taxes to be paid, health care expenses, and retirement income as part of the plan. When these components are given thoughtful consideration beforehand, it will help ensure that your golden years are successful financially speaking.

What to do 3 months before retirement?

Three months before retirement, meet with a retirement specialist to review benefits, decide which coverage to choose, and begin enrollment paperwork. Confirm whether payroll deductions can be continued and check eligibility for health and dental coverage.

Get an estimate of your monthly Social Security benefit and determine plans for healthcare and Medicare coverage.

What are the signs that you are ready to retire?

When you’re ready to retire, it’s important to make sure that you have a diverse financial portfolio in place and no debt. There should be plans for social security benefits as well as health care coverage and any potential unforeseen expenses. By having these measures in place, your retirement will feel secure financially so that you can focus on enjoying yourself after years of hard work!

What is the 3% rule in retirement?

In retirement, it is often advised to use the Three Percent Rule as a guideline when withdrawing money from one’s portfolio. This rule states that no more than 3% of your initial total should be taken out annually in order for the funds to last and take into consideration inflation rates. Retirement can have financial stability if this principle is followed, giving security during such an important life stage.

What is the $ 1,000-a-month rule for retirement?

The $1000-a-month rule is a retirement guideline stating that for each month of income desired in retirement, individuals need to save around $240,000. Thus, with the aim of having monthly earnings at the level of $3,000 during their post-working years requires setting aside approximately 720K.

Related Articles

Traditional IRA vs. Roth IRA

Traditional Individual Retirement Accounts (IRA), which were created in 1974, are owned by roughly 36.1 million U.S. households. And Roth IRAs, created as part of the Taxpayer Relief Act in

Peter Foldes

Nov, 10 2021

Tax Efficiency in Retirement

Will you pay higher taxes in retirement? It’s possible. But that will largely depend on how you generate income. Will it be from working? Will it be from retirement plans?

Peter Foldes

Nov, 10 2021

Consider Keeping Your Life Insurance When You Retire

Do you need a life insurance policy in retirement? One school of thought questions this decision. Perhaps your kids have grown and the need to help protect the household against

Peter Foldes

Nov, 10 2021