“Retirement is wonderful if you have two essentials – much to live on and much to live for.” -Unknown

What do tax brackets have to do with retirement? If you have never thought about this concept, it’s time to buckle up because we’ll tell you all about it and how it affects your retirement score!

Tax brackets play a significant role in retirement planning because they directly impact how much tax you’ll owe on your income during retirement. This is why it’s important to learn about their function in ascertaining the amount of tax payable according to one’s earnings and examining the influence they have on your taxation.

Key Takeaways

- Keep up with 2024 IRS updates. The IRS has updated the 2024 tax brackets, maintaining the same tax rates but adjusting income thresholds, which impact how much tax is owed based on income levels.

- Higher income has higher taxes. Federal income tax operates on a progressive system where higher income portions are taxed at higher rates, resulting in a blended tax rate rather than applying the highest rate to the entire income.

- Understanding the difference between marginal and effective tax rates is crucial for tax planning. The marginal rate applies to your highest income portion, while the effective rate is the average tax rate on your total income.

Understanding 2024 Federal Income Tax Brackets

The Internal Revenue Service has revised the income thresholds for federal tax brackets in 2024 while keeping the same seven rates of taxation. These tax brackets are utilized to ascertain which portion of a taxpayer’s income is subject to their respective federal income tax rate during that year.

The following percentages represent these established rates:

- 10%

- 12%

- 22%

- 24%

- 32%

- 35%

- 37%

These percentage points correspond with varying levels of taxable earnings.

Your first few dollars of income are taxed at 10%.

For single filers, income up to $11,600 is also taxed at 10%. For married couples filing jointly, this rate applies to income up to $23,200. If you’re a head of household, the 10% rate covers income up to $16,550.

As you earn more, you’ll move into higher tax brackets.

For example, if you’re single and make between $11,601 and $47,150, you’ll fall into the 12% tax bracket. Heads of households with income between $16,551 and $63,100 are also taxed at 12%.

How Federal Income Tax Brackets Work

In the U.S., the federal income tax system is progressive, meaning the more you earn, the higher your tax rate. Your taxable income, which includes wages and other earnings, along with your filing status, determines which tax brackets apply to you.

Here’s the key: Only the income over certain thresholds is taxed at higher rates, not your entire income.

Let’s break it down with an example. If you’re single and have a taxable income of $50,000, here’s how it works:

- The first $11,600 is taxed at 10%.

- The income from $11,601 to $47,150 is taxed at 12%.

- Any amount above $47,150 is taxed at 22%.

So, only the money over $47,150 gets the 22% rate. This tiered system means you don’t pay the highest rate on all your income.

Understanding how these brackets work can clear up common misconceptions. Many people think they pay the highest tax rate on their entire income, but that’s not true.

Instead, each part of your income is taxed at its lower corresponding rate, often resulting in a lower overall tax burden than you might expect.

Marginal vs. Effective Tax Rates

In tax-related discussions, the terms marginal tax rate and effective tax rate frequently arise. The marginal tax reader indicates the proportion of taxation applied to your highest tier of taxable income.

This rate escalates when an individual’s income increases and segments of that income move into steeper brackets. For example, if you earn one more dollar that is taxed at 22%, then your marginal tax rate stands at 22%.

Conversely, the effective tax rate calculates the average percentage of your entire earnings subjected to taxes. It’s determined by taking your whole annual gross revenue and dividing it by what you owe in taxes for that year.

Take an illustration where a person has a $50,000 total yearly earnings with a corresponding $6,000 in taxes, resulting in an effective tax figure standing at 12%. Due mainly to our stepped or progressive framework within which we’re taxed.

This number typically lands under their respective top-most margin range.

Comprehending these distinct figures—marginal versus as compared to overall—is crucial for precision during financial strategizing associated with taxes. While considerations regarding any additional earnings should take into account one’s uppermost payment slab, i.e., their boundary level impacts each next unit earned separately.

Meanwhile, visualizing someone’s complete load stresses more upon one’s full portrayal via reflecting such condensed weighted overview rates on every point gathered cumulatively all along.

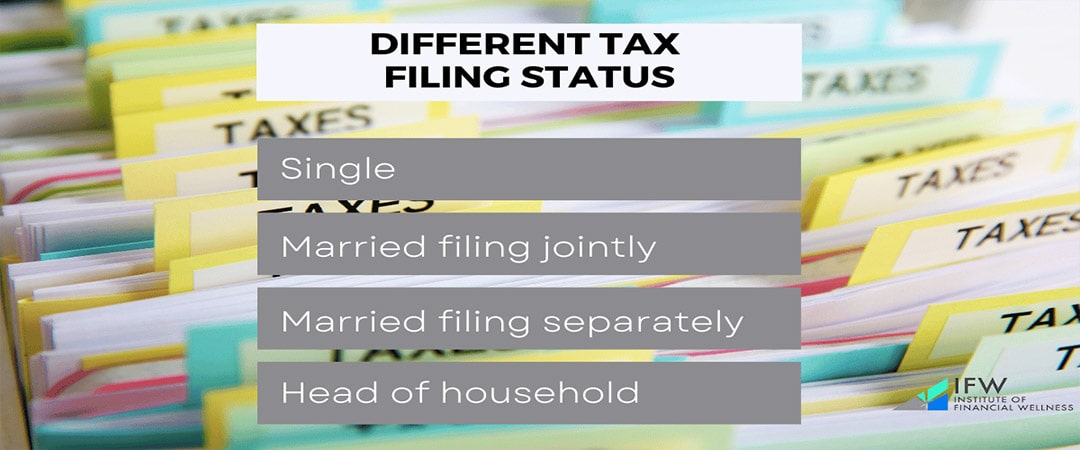

Filing Status and Its Impact on Tax Brackets

Choosing the right filing status can save you money on taxes.

When it comes to federal income taxes, the filing status you select significantly affects your tax brackets and rates. The main filing statuses are:

- Single

- Married Filing Jointly

- Married Filing Separately

- Head of Household

Each status has different income thresholds for each tax bracket, which can greatly impact how much you owe.

For example, let’s consider a married couple filing jointly with a taxable income of $120,000. Their income would fall into the 22% tax bracket because this portion of their earnings fits within the range for that rate.

However, if a single person earns the same $120,000, their marginal tax rate might be different due to the different brackets for single filers.

Choosing the right filing status isn’t just a matter of categorization; it’s essential for managing your tax liability effectively. Your filing status influences not only the tax rates applied to your income but also your eligibility for various credits and deductions.

This can significantly affect your total tax bill when it’s time to pay up.

Strategies to Lower Your Taxable Income

Want to pay less in federal taxes? By lowering your taxable income, you can reduce your overall tax bill and potentially move into a lower tax bracket.

Here’s how you can do it:

1. Use Tax Deductions: Deductions lower your taxable income, which can reduce the amount of income that falls into higher tax brackets. Common deductions include:

- Charitable Contributions: Donations to qualifying organizations can be deducted from your taxable income.

- Property Taxes: You can deduct state and local property taxes on your home.

- Home Mortgage Interest: The interest paid on your home mortgage is often deductible.

2. Take Advantage of Tax Credits: Unlike deductions, credits reduce your tax bill directly, dollar-for-dollar. Some popular credits include:

- Child Tax Credit: Provides a credit for each qualifying child.

- Earned Income Tax Credit: This helps low- to moderate-income workers reduce their tax bill.

Using these strategies effectively can lower the amount of your income that’s taxed and might even drop you into a lower tax bracket. This means paying less in taxes overall.

We’ll dive deeper into these methods in the next sections to show you how to maximize your savings.

Utilizing Tax Deductions

Using deductions is a powerful way to reduce your taxable income. By subtracting certain expenses, such as charitable donations, property taxes, and mortgage interest, from your earnings, you can decrease the amount subject to federal taxation.

Here’s how it works:

- Charitable Contributions: Donating to qualified charities allows you to deduct the amount from your taxable income.

- Property Taxes: You can deduct state and local property taxes paid on your home.

- Mortgage Interest: The interest paid on your mortgage is deductible, reducing your taxable income.

Additionally, contributing to a Health Savings Account (HSA) allows for deductions on the contributions made, and withdrawals for eligible healthcare costs are tax-free.

For self-employed individuals, deductions can be significant. They can deduct expenses like home office costs, provided the space is used exclusively for business purposes.

Keep in mind that deductions for IRA contributions start phasing out above certain adjusted gross income thresholds, especially if you participate in other retirement savings plans.

Understanding these deductions can help you effectively lower your taxable income and potentially reduce your tax bill.

Claiming Tax Credits

Tax credits are a powerful way to reduce your tax liability directly, potentially leading to a refund if credits exceed your tax owed. Here’s how they work:

- Child Tax Credit: You can deduct up to $2,000 per eligible child. Starting in 2024, the refundable portion of this credit will increase to $1,700, which means you may receive a refund even if you owe no taxes.

- Earned Income Tax Credit (EITC): This credit provides substantial benefits, especially for taxpayers with three or more children. It can amount to up to $7,830, depending on your income and family size.

- American Opportunity Tax Credit: Designed for qualifying students, this credit can provide up to $2,500 annually to help cover education expenses.

- Lifetime Learning Credit: Offers a credit of up to 20% on qualified education expenses, with a maximum credit of $2,000 per tax return.

Utilizing these credits effectively can significantly reduce your tax bill or even result in a refund. They are valuable tools for managing your tax liability and should be explored based on your specific financial situation and eligibility criteria.

Inflation Adjustments and Their Effect on Tax Brackets

How does inflation affect the tax system? Each year, the IRS updates tax brackets to account for changes in the cost of living caused by inflation.

This ensures that taxpayers aren’t pushed into higher tax brackets simply due to increases in prices, a phenomenon known as bracket creep. These adjustments help maintain the real value of credits and deductions.

For example, in 2021, the income threshold for single filers in the lowest 10% tax bracket increased from $9,875 to $9,950 due to these annual adjustments. By making these changes regularly, the tax system accurately reflects economic shifts without unfairly burdening taxpayers.

The IRS announces these adjustments annually, along with updated rate schedules and other modifications, which will apply starting in the 2024 tax year.

Even though tax rates themselves may remain unchanged, your actual personal tax rate could be affected by these yearly adjustments to brackets, as well as changes to deductions or credits. This highlights the importance of staying informed about these updates when planning your financial strategies around taxes.

Special Considerations for High-Income Earners

Is it the same for high-income individuals? The answer is no.

Individuals with higher incomes face specific tax challenges and opportunities. Converting SIMPLE, SEP, or traditional IRAs to Roth IRAs can be advantageous because qualified withdrawals from Roth accounts are not subject to federal income tax.

Investing in tax-exempt bonds is another strategic move, as the interest they generate is not taxable at the federal level and may also be exempt from certain state income taxes.

For these earners, contributing to a Health Savings Account (HSA) is beneficial due to its tax-free contributions and earnings growth. The Alternative Minimum Tax (AMT), designed to prevent high-income individuals from avoiding taxes entirely, applies in these cases.

By 2024, exemptions for the AMT will rise to $85,700 for single filers and up to $133,300 for married couples filing jointly.

Calculating Your Federal Income Tax Liability

To calculate your federal income tax liability, follow these steps:

- Determine your taxable income by subtracting any deductions from your adjusted gross income (AGI). Deductions can be itemized, or you can choose the standard deduction.

- Note that for 2024, the standard deduction increases by $750 for single filers and by $1,500 for joint filers.

- Use IRS-provided tax tables based on your filing status to find the applicable tax rates for different segments of your taxable income. Your total taxable income is divided into portions according to each tax bracket, and you apply the corresponding rates to each segment.

For example, if your taxable income is $50,000, you would apply the appropriate bracket percentages cumulatively. This calculation could result in a total tax owed of approximately $17,656.

Understanding these calculations is crucial for accurately estimating your federal tax obligation and identifying potential opportunities to reduce your tax liability through strategic financial planning.

Historical Perspective on Tax Brackets

Since their inception in 1913 to support wartime efforts, federal tax brackets have undergone significant changes. The top tax rate skyrocketed to a high of 77% by the end of World War I, peaking even further to an unprecedented 94% during World War II.

Over time, there has been a gradual reduction in these rates, notably during the Reagan administration in the 1980s. More recently, the Tax Cuts and Jobs Act of 2017 ushered in another period of lower individual federal tax rates for a limited duration.

Currently, the maximum federal tax bracket stands at 37%, down from its previous level of 39.6% in 2013. This evolution highlights how economic shifts and policy decisions can shape taxation policies over the years.

Common Mistakes to Avoid When Filing Taxes

Tax filing can be complex, often leading to common mistakes that can impact your return. To avoid errors:

- Accurate Personal Data: Ensure names are spelled correctly and social security numbers are accurate. Mistakes here can delay processing or lead to rejection of your return.

- Banking Details: Double-check banking information for electronic refunds to avoid delays or complications in receiving your refund.

- Declare All Income: Don’t forget to report all sources of income, including earnings from part-time jobs or freelance work. Failure to do so can result in penalties for underpayment of taxes.

- Properly Categorize Earnings: Classify income correctly to avoid issues with underpayment and potential fines or interest charges.

Avoiding these pitfalls can streamline your tax filing experience and help ensure accurate submission of your taxes.

Empowering Financial Futures: The Institute of Financial Wellness and its Comprehensive Education Platform

The Institute of Financial Wellness (IFW) serves as an expansive multi-media platform that delivers financial education, tools, and services to the public. Our mission is to guide individuals toward financial health by offering compelling and educational material.

Among our diverse array of resources are e-newsletters, the Retirement Score Webinar, and on-demand video services that supply critical insights into finance.

Key among IFW’s offerings is the IFW Retirement Roadmap—a tool explicitly crafted to help people fulfill their retirement aspirations without fear of depleting funds or suffering from market fluctuations and unwarranted taxes. It advises how best to utilize 401(k) plans effectively as well as strategies for life/disability insurance coverage and saving for higher education expenses.

By providing accessible financial learning opportunities customized to each person’s unique circumstances, IFw strives in making sure personal finances can be handled with confidence. This initiative positions the institute as a premier resource for anyone seeking ways to enhance their fiscal status.

Full Summary

Understanding the intricacies of the IRS tax rate schedules and how they affect your retirement planning is crucial for your financial well-being. We’ve explored the 2024 federal income tax brackets, how these brackets work, and the difference between marginal and effective tax rates.

We’ve also discussed the impact of filing status, strategies to lower your taxable income, and the importance of inflation adjustments. For high-income earners, special considerations such as Roth IRA conversions and tax-exempt bonds can provide significant tax benefits.

By avoiding common tax filing mistakes and utilizing resources like the Institute of Financial Wellness, you can make informed decisions that enhance your financial security. Whether you are preparing for retirement or managing your current tax situation, these insights and strategies can help you navigate the complex tax landscape with confidence.

Frequently Asked Questions

What are the 2024 federal income tax brackets?

In 2024, there are seven federal income tax brackets, with rates starting at 10% and escalating up to 37%. These brackets correspond to diverse income thresholds that apply according to the taxpayer’s filing status.

how many tax returns were filed in 2021?

In 2021, taxpayers submitted 153.6 million tax returns, reporting over $14.7 trillion in adjusted gross income (AGI) and paying close to $2.2 trillion in individual income taxes [1].

How does the marginal tax rate differ from the effective tax rate?

The effective tax rate represents the average percentage taken from your entire income as tax, whereas the marginal tax rate is applied only to the last and highest portion of your earnings. Essentially, while your total income is subject to the effective tax rate, it’s only that final dollar earned that is taxed at the marginal tax rate.

How much was collected in taxes in 2023?

During Fiscal Year (FY) 2023, the IRS collected nearly $4.7 trillion in gross taxes. This substantial revenue comes from various sources, including individual income taxes, corporate taxes, and other forms of taxation. If you lived or worked in the United States in 2023, your tax contributions are likely part of this significant amount [2].

How does filing status affect my tax bracket?

The tax brackets you fall into and the corresponding rates are directly influenced by your filing status, which sets specific income thresholds. This relationship is crucial as it determines your total tax liability. Varying statuses yield different thresholds for identical tax rates, affecting the amount of taxes you’re required to pay.

What are some strategies to lower my taxable income?

Consider taking advantage of tax deductions, including those for charitable contributions and mortgage interest, along with claiming credits such as the Earned Income Tax Credit and Child Tax Credit to decrease your taxable income. Employing these tactics can effectively reduce the portion of your income that is liable to income tax.

Where there people who did not pay taxes in 2023?

In 2023, tens of millions of Americans owed little or no federal income tax. Here’s a breakdown:

- No AGI (Taxable Income): The IRS received nearly 5.3 million individual tax returns showing no AGI, which means no taxable income.

- AGIs Under $30,000: Another 60.3 million returns had AGIs less than $30,000. The average effective tax rate for these taxpayers was 1.5%, even before applying refundable tax credits [3].

What is bracket creep, and how do inflation adjustments help?

Bracket creep occurs when inflation drives incomes into higher tax brackets, which results in an increased tax liability even though there hasn’t been an actual rise in real income.

To counteract this effect, the IRS makes yearly adjustments to the income thresholds to reflect changes in living costs.

Related Articles

Tax Efficiency in Retirement

Will you pay higher taxes in retirement? It’s possible. But that will largely depend on how you generate income. Will it be from working? Will it be from retirement plans?

Peter Foldes

Nov, 10 2021

What Is a 1035 Exchange?

According to the most recent information available, Americans have individual life insurance with a total face value of $12.4 trillion.1 Due to a variety of factors, these individuals may find

Peter Foldes

Nov, 10 2021

Important Tax Return Deadlines for 2021 Returns

Here is an overview of deadline dates, return types, dates to receive your forms, extensions, etc., and a brief description with helpful tips. Make sure you adhere to the deadlines

Peter Foldes

Dec, 02 2021