“Retirement is not a life without purpose; it is the ongoing purpose that provides a meaningful life.” -Robert Rivers

Concerned about health care costs in retirement? A 65-year-old couple might need $383,000, depending on their retirement score.

We are ready to help you estimate these costs, understand Medicare parts, and use financial tools like HSAs to keep your retirement health expenses under control. The question is… are you ready?

Key Takeaways

- Accurately estimating healthcare costs in retirement is essential. A healthy 65-year-old couple potentially needs approximately $383,000 for medical expenses, which could consume a significant portion of their lifetime Social Security benefits.

- Understanding Medicare’s parts and coverage limitations is crucial for effective retirement planning. Medicare Parts A and B cover hospital and medical services but exclude long-term care, vision, hearing, dental care, and medical care outside the U.S.

- Health Savings Accounts (HSAs) are powerful tools for managing medical expenses in retirement. They offer triple tax benefits, such as: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

Estimating Health Care Costs in Retirement

Thinking about healthcare costs in retirement is crucial to protect your savings. If you’re a healthy couple retiring at 65 this year, you might need about $383,000 to cover medical expenses. Shockingly, this could eat up nearly 70% of your Social Security benefits over your lifetime. And since medical costs are rising faster than inflation, this number is likely to grow.

To stay financially secure, consider these tips:

- Start Saving Early: Put aside a lump sum or increase your regular contributions now.

- Explore Health Savings Options: Look into Health Savings Accounts (HSAs) and long-term care insurance.

- Plan for Medicare Gaps: About a third of your health costs won’t be covered by Medicare. Save for those extra expenses like premiums and deductibles.

Creating a solid plan for these costs will help keep you financially secure during retirement.

Understanding Medicare Coverage

Understanding Medicare is also very important for your healthcare in retirement.

Medicare is the federal health insurance program for people 65 and older. It has four parts, each covering different healthcare needs:

- Part A: Hospital Insurance – This type of insurance covers inpatient hospital stays, some skilled nursing facilities, hospice care, and home health care.

- Part B: Medical Insurance – Helps pay for doctors’ services, outpatient care, medical supplies, and preventive services.

- Part C: Medicare Advantage Plans – An alternative to Original Medicare that includes Parts A and B and often additional benefits.

- Part D: Prescription Drug Coverage – Helps cover the cost of prescription medications.

However, Medicare does not cover long-term care, vision, dental, hearing services, or international medical treatment.

Knowing what each part of Medicare covers helps you plan your healthcare needs in retirement. Let’s get into it!

Original Medicare (Parts A & B)

Known as Traditional Medicare or Fee-for-Service (FFS) Medicare, Original Medicare is made up of Part A and Part B.

Part A covers:

- stays in an inpatient hospital

- skilled nursing care

- healthcare at home

- hospice services

This coverage plays a pivotal role since expenses related to hospital admissions can become one of the most significant medical costs during retirement.

Conversely, Part B provides for outpatient and physician services, including consultations with doctors and preventive measures. Despite its broad service coverage, there is a monthly premium attached to it – $174.70 as of 2024.

It’s important to note that while many benefits fall under Part B’s umbrella, it doesn’t extend to all possible healthcare needs. Being aware of these limitations allows you to arrange for supplemental insurance or allocate savings specifically for those uncovered services.

Medicare Advantage Plans (Part C)

Medicare Advantage (Part C) is a broader coverage option.

It is an alternative to Original Medicare offered by private insurance companies. It covers everything in Part A (hospital insurance) and Part B (medical insurance) and often adds extra benefits like dental, hearing, and vision care, which Original Medicare doesn’t cover.

If you’re looking for more comprehensive coverage, Medicare Advantage might be a good choice. Here’s what to consider:

- More Benefits: These plans can offer broader coverage, including dental, vision, and hearing.

- Cost Comparison: While Medicare Advantage may cover more services, it might come with higher premiums or increased out-of-pocket expenses compared to Original Medicare.

Carefully weigh the benefits and costs of Medicare Advantage against your current plan to see what fits your needs best.

Prescription Drug Coverage (Part D)

Medicare Part D is your key to affordable prescription medications. Unlike Original Medicare, which doesn’t cover prescriptions, Part D provides this through private drug plans (PDPs).

Here’s why Part D is important:

- Cuts Your Costs: By enrolling in a Part D plan, you can significantly reduce the money you spend out-of-pocket on medications.

- Affordable Options: In 2024, monthly premiums for Part D plans range from $12.90 to $81.55.

To make the most of Part D, check your medications: Make sure the plan you choose covers the drugs you need regularly.

Choosing the right Part D plan helps you manage prescription costs effectively, leaving more of your retirement savings for other needs.

Utilizing Health Savings Accounts (HSAs)

A Health Savings Account (HSA) is your retirement healthcare ally! This is a powerful way to manage medical expenses and reduce your taxable income. HSAs offer a triple tax advantage:

- Tax-Free Contributions: Money you put into an HSA is tax-free.

- Tax-Free Growth: Your balance grows without being taxed.

- Tax-Free Withdrawals: When used for qualified medical expenses, withdrawals aren’t taxed.

Here’s how you can benefit from an HSA if you have a high-deductible health plan:

- Save for the Future: Allocate funds tax-free for future medical costs.

- Rollover Benefits: Unlike Flexible Spending Accounts (FSAs), any unused funds carry over year after year.

- Ownership Flexibility: You keep your HSA even if you change jobs or retire.

To maximize your HSA:

- Contribute Fully: Aim to contribute up to the annual legal maximum.

- Track Expenses: Save your receipts for medical expenses so you can reimburse yourself tax-free later.

Using an HSA wisely can significantly ease healthcare costs during retirement.

Planning for Long-Term Care

Almost 70% of people who turn 65 today will need some form of long-term care during their lifetime. Planning ahead is essential to manage this possibility, whether it’s due to aging or ongoing health issues.

Understanding your options and their costs will help you make informed decisions while you’re still able.

Types of Long-Term Care:

- Informal Care: Family and friends can provide help at home.

- Professional Help: Hire nurses or home health aides for in-home care.

- Community-Based Services: Use adult day care centers or senior centers for meals, activities, and personal care.

- Residential Care: Move to assisted living facilities or nursing homes for full-time care, activities, and meals.

How much does care cost? A private room in a nursing home costs about $108,405 per year on average, and this is how you can financially prepare:

- Long-Term Care Insurance: This type of policy helps cover the costs of living assistance and nursing home care.

- Life Insurance with Riders: Policies that include riders for chronic illnesses can help cover long-term care expenses.

- Hybrid Policies: These combine life insurance with long-term care benefits, offering a flexible way to manage costs.

When is it best to start planning? It’s best to consider these options in your 50s or early 60s.

Early planning can save you money and protect your retirement savings from high healthcare costs.

Planning for long-term care can help you stay financially secure and ensure you receive the care you need later in life.

Managing Modified Adjusted Gross Income (MAGI)

Keep your Medicare costs low by managing your MAGI. It is key to keeping Medicare premiums affordable and qualifying for financial assistance with healthcare.

If your MAGI exceeds certain thresholds, you’ll face an extra charge called the Income-Related Monthly Adjustment Amount (IRMAA) for Medicare Parts B and D. Staying under these limits can save you a lot on your monthly Medicare premiums.

Tips to Lower Your MAGI:

- Max Out Retirement Contributions: Fully fund your 401(k) or traditional IRA. Contributions to these accounts are made with pre-tax dollars, reducing your taxable income.

- Offset Capital Gains: Sell investments that have lost value to offset any gains. This can lower your overall taxable income.

By using these strategies, you can manage your MAGI effectively, making your healthcare expenses more manageable in retirement.

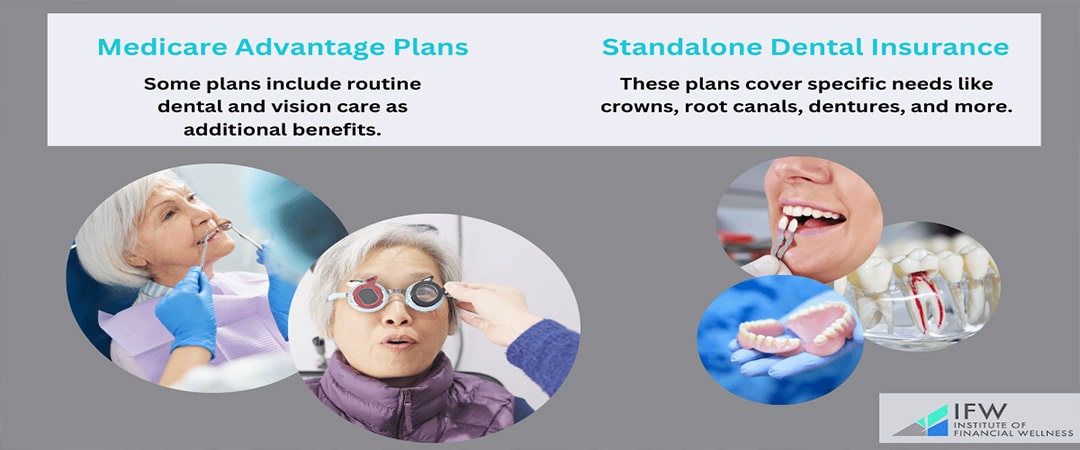

Preparing for Dental and Vision Expenses

Don’t overlook dental and vision care in retirement! They’re often neglected in financial planning.

Many seniors face gum disease and other oral issues, highlighting the importance of regular dental visits. Surprisingly, more than 25% of seniors haven’t seen a dentist in the last five years, emphasizing the need for dental insurance [1].

Options for Coverage:

- Medicare Advantage Plans: Some plans include routine dental and vision care as additional benefits.

- Standalone Dental Insurance: These plans cover specific needs like crowns, root canals, dentures, and more.

By preparing for these expenses, you can avoid unexpected costs and better maintain your health in retirement. Don’t forget to include dental and vision care in your financial plans for a secure and healthy future.

Health Insurance Options Before Medicare Eligibility

Navigating health insurance options before becoming eligible for Medicare is crucial for retirees. While some employers offer post-retirement healthcare benefits, only about 21% of large employers provide this coverage [2].

Retirees may extend their employer-backed health plan for up to 18 months through COBRA, but this often results in higher premiums.

Alternatively, retirees might opt to remain covered under a spouse’s employer-based policy or explore purchasing individual private insurance. High-deductible health plans paired with Health Savings Accounts (HSAs) offer lower premiums but higher out-of-pocket expenses.

For those aged 55 to 64, government-operated insurance marketplaces provide another avenue, with this demographic representing over a quarter of all plan purchases.

Financial Strategies to Cover Health Care Costs

Are there any financial tactics that can be employed? Yes! Key approaches include:

- Drawing on retirement savings

- Making use of Health Savings Accounts (HSAs) and other accounts with tax benefits

- Capitalizing on Flexible Spending Accounts (FSAs), which provide a tax-favored method for covering qualified medical expenses

Employing these methods will help establish a robust monetary base to address your health-related needs upon retiring.

Engaging the services of a financial advisor proves invaluable when it comes to projecting future healthcare expenditures and formulating an all-encompassing plan for handling these costs. Utilization of both sound fiscal instruments and expert guidance equips you better in anticipating and tackling the inevitable healthcare expenses associated with retirement.

Working with a Financial Advisor

In the course of retirement planning, a financial advisor is instrumental in helping you navigate your healthcare expenses. They frequently employ projections for healthcare costs that anticipate a 4.5% rate of inflation, enabling you to devise a more accurate and effective strategy.

By reviewing your historical healthcare spending patterns, these professionals can forecast impending expenditures and seamlessly integrate them into your anticipated retirement budget.

Collaborating with a financial advisory service provides the advantage of developing an exhaustive strategy tailored to address healthcare expenditures as part of your overall fiscal plan during retirement years. Such proactive planning affords you tranquility.

It assures that not only are all potential health-related needs accounted for but also safeguards against any undue strain on your economic stability post-retirement.

Achieve Financial Success with the Institute of Financial Wellness

The Institute of Financial Wellness (IFW) stands as a premier all-inclusive platform for financial instruction, resources, and services delivered through multimedia. We are dedicated to empowering individuals by providing clear and assured guidance for sound financial choices.

The IFW delivers an array of engaging content tailored to enhance financial literacy, which includes webinars, videos on demand, and electronic newsletters.

For those approaching retirement or already navigating it, the IFW Retirement Roadmap and our Retirement Score Webinar are invaluable tools designed to alleviate concerns about depleting funds while securing retirement assets against the uncertainties of market fluctuations. The IFW offers a comprehensive financial check-up that assesses your fiscal well-being in areas such as budgeting techniques and meeting savings objectives.

Engaging with an IFW Financial Professional means personalized recommendations and strategies are formulated just for you. Leveraging a cadre of proficient experts equipped with esteemed credentials ensures that the IFW is well-positioned to offer continuous advice and steadfast support systems designed to optimize your monetary achievement throughout every chapter of your life journey.

Full Summary

To effectively handle healthcare expenses during retirement, it’s essential to take a comprehensive approach. This involves gaining a solid grasp of what Medicare covers, making good use of Health Savings Accounts (HSAs), preparing for the potential need for long-term care, and seeking guidance from a financial advisor.

Engaging in proactive preparation is crucial to ensure that you can have both financial stability and good health in your later years. Starting early and maintaining an informed perspective are fundamental to managing the costs associated with healthcare after retirement successfully.

Frequently Asked Questions

How much should I expect to spend on healthcare in retirement?

A healthy couple aged 65 should anticipate healthcare expenses amounting to roughly $383,000 during retirement.

What does Original Medicare cover?

Original Medicare, which encompasses Parts A and B, provides coverage for services that include inpatient hospital care, outpatient medical assistance, skilled nursing facility stays, home healthcare provisions, and hospice support.

It does not extend its coverage to include prescription drugs.

How many Americans over 65 have health insurance?

In 2021, 34.2 percent of individuals aged 65 and older had healthcare coverage through Medicare Advantage. Privately insured individuals, with or without Medicare, constituted the largest group among older adults in the U.S., while the uninsured accounted for only 0.5 percent of this demographic.

These figures depict the distribution of health insurance coverage among adults aged 65 and above in the U.S. in 2021 [3].

Can I use Health Savings Account (HSA) funds after I enroll in Medicare?

Certainly, after enrolling in Medicare, you are still allowed to utilize funds from your HSA for qualified medical expenses. It is important to note that at this point you will not be permitted to add additional contributions to the HSA.

What are my options for long-term care?

You should evaluate every possibility for long-term care based on your unique requirements and personal desires. These options encompass care within the home, support services in community settings, accommodations at residential establishments, insurance policies specifically tailored for long-term care needs, as well as life insurance policies that include riders for long-term care.

How can I reduce my Modified Adjusted Gross Income (MAGI)?

Consider lowering your Modified Adjusted Gross Income (MAGI) by fully funding retirement accounts and health savings accounts, along with divesting from taxable investments that are at a loss. Implementing these tactics can effectively decrease your taxable income.

Related Articles

Tax Efficiency in Retirement

Will you pay higher taxes in retirement? It’s possible. But that will largely depend on how you generate income. Will it be from working? Will it be from retirement plans?

Peter Foldes

Nov, 10 2021

What Is a 1035 Exchange?

According to the most recent information available, Americans have individual life insurance with a total face value of $12.4 trillion.1 Due to a variety of factors, these individuals may find

Peter Foldes

Nov, 10 2021

Important Tax Return Deadlines for 2021 Returns

Here is an overview of deadline dates, return types, dates to receive your forms, extensions, etc., and a brief description with helpful tips. Make sure you adhere to the deadlines

Peter Foldes

Dec, 02 2021