The future of Social Security is uncertain, with funds potentially depleting by 2033. What does this mean for your retirement score? This article examines the possible changes, impacts on different income groups, and strategies to secure your financial stability.

You can also visit our retirement webinar for a free discussion about your retirement security.

Key Takeaways

- The impending depletion of the Old Age and Survivors Insurance (OASI) Trust Fund by 2033 and the projected shortfall in Social Security benefits necessitate legislative amendments and thoughtful financial planning to ensure sustainability.

- Wealthy retirees might face unique challenges due to changes in Social Security, despite higher benefits; changes like increased payroll taxes could affect their income, requiring strategic preparation to maintain financial security.

- Diversifying retirement income and maximizing employer contributions are crucial strategies for mitigating risks associated with potential Social Security changes, thereby securing a more stable financial future.

Understanding the Future of Social Security

Let’s get down to it. How can we plan for a secure retirement if we don’t know the future of social security? Growing fears about Social Security’s future have many Americans deeply worried about its long-term sustainability.

The Old Age and Survivors Insurance (OASI) Trust Fund, which pays benefits to retirees and their families, is projected to deplete by 2033, while the Disability Insurance (DI) Trust Fund is expected to remain solvent through at least 2098.

This timeline emphasizes the need to comprehend the present state of Social Security and its future projections.

The financial health of the Social Security program is influenced by various factors, including population aging and decreased birth rates.

- As the large baby boom generation retires, the ratio of beneficiaries to workers paying into the system shifts, leading to a shortfall in the program’s financial status.

- By 2035, it is projected that revenue from Social Security taxes will only cover 75% of scheduled benefits.

Projected Depletion Dates

If you’re worried about the future of Social Security, you are not alone. It is top of mind for all retirees and anyone who is taking retirement planning seriously.

The combined Old Age and Survivors Insurance (OASI) and Disability Insurance (DI) Trust Funds are expected to deplete by 2035.

- Specifically, the OASI Trust Fund reserves will be exhausted by 2033, after which continuing income will only cover about 75% of scheduled benefits.

- For the Disability Insurance Trust Fund, the outlook is more stable, with projections showing full benefits being paid through at least 2098.

- However, the overall shortfall expected by 2037 suggests that without significant changes, beneficiaries could face reduced payments.

Legislative Proposals

What is Government trying to do about it all?

Several legislative proposals aim to address the possible Social Security shortfall. One prominent suggestion is eliminating the income cap on Social Security taxes, which could address 73% of the long-term shortfall.

This measure has garnered significant public support, reflecting a collective willingness to sustain the Social Security system.

Another proposal involves means-testing benefits, which would adjust benefit formulas based on the recipient’s income.

Historically, lawmakers have implemented changes such as:

- Increasing the payroll tax rate

- Raising the retirement age to maintain the program’s solvency

Current proposals continue this trend, with suggestions to:

- Increase payroll tax rates

- Reduce benefits

- Raise the full retirement age

The Social Security Board of Trustees regularly reviews these proposals, emphasizing the need for timely action to prevent significant benefit reductions.

Impact on Benefits

Potential changes to Social Security are likely to impact various groups differently.

For example:

- If the OASI Trust Fund reserves deplete by 2033, continuing income will only cover 79% of scheduled benefits.

- By 2037, this figure could drop to 76%, highlighting the need for immediate legislative action to prevent considerable benefit reductions.

- These reductions will disproportionately affect low-income workers and minority groups who rely heavily on Social Security for their retirement income.

- The primary insurance amount (PIA) formula, which determines Social Security benefits, offers higher benefit replacement rates for low-income workers compared to their higher-income counterparts.

This design aims to provide a more significant safety net for those with lower lifetime earnings.

However, the potential reductions in benefits underscore the importance of working for at least 35 years to maximize the average benefit calculation and ensure they pay scheduled benefits.

How Will Wealthy Retirees Be Affected by Changes?

Changes to Social Security will inevitably affect different economic groups in varied ways. Individuals nearing retirement are particularly vulnerable, with less time to adjust their financial plans.

At the same time, wealthy retirees, although receiving more substantial Social Security checks, might face different challenges compared to their middle-class counterparts.

Gaining insight into the effects of these changes on each group can enable retirees to plan more effectively.

Low-income workers and minority groups, who depend more significantly on Social Security due to lower lifetime earnings and fewer retirement savings, will be the most affected.

For the wealthy and middle-class retirees, the strategies to navigate these changes might seem different but equally crucial. We should explore the unique challenges and strategies applicable to each group.

Nearing Retirement

Individuals nearing retirement age face significant challenges due to potential changes in Social Security benefits.

- With less time to adjust their financial plans, these individuals may find it difficult to compensate for any shortfalls in expected benefits. Many have planned their finances around anticipated Social Security payments, making sudden changes particularly disruptive.

- The projected increase in poverty rates among Social Security beneficiaries aged 60 and older further underscores the urgency of addressing these issues.

- As potential benefit cuts loom, it becomes vital for those nearing retirement to reassess their savings and explore alternative income sources to secure their financial future.

The Wealthy

Wealthy retirees, who receive more substantial Social Security benefits due to higher lifetime earnings, face a unique set of challenges. Although their benefits are higher, changes in the Social Security system, such as increased payroll taxes or benefit adjustments, could affect their retirement income.

- For instance, individuals stop paying into Social Security once their income reaches $168,600 or more, meaning high earners contribute a smaller percentage of their income compared to lower earners.

- Despite receiving higher benefits, the effective tax rate for millionaires can be less than 1%.

- This discrepancy underlines the importance of reconsidering how contributions are calculated and making sure that individuals with substantial incomes contribute equitably to the system.

The Middle-Class

Middle-class retirees often rely heavily on Social Security retirement benefits as a primary source of income.

- In fact, 69% of middle-class beneficiaries receive social security benefits, which provide more than half of their total income.

- Married couples and unmarried beneficiaries alike depend on these payments to sustain their standard of living.

- Given that retirees need approximately 70%-80% of their pre-retirement income to maintain their lifestyle, and Social Security benefits only replace around 40%, any reductions in benefits could severely impact their financial security.

Preparing for Potential Changes

Given the possible changes to Social Security, adopting proactive strategies to secure your retirement is essential.

Planning for less generous retirement benefits and diversifying your income sources can help mitigate the impact of any reductions.

Consulting a financial advisor can provide personalized strategies to enhance your retirement planning.

Starting to save early, diversifying your retirement income, and maximizing employer contributions are key steps in preparing for potential changes.

If You Haven’t Saved, Start Now

For those who haven’t started saving for retirement, now is the time to prioritize it.

Despite the concern, it is not too late to act and improve your financial situation. Even for late savers, it’s possible to accumulate a significant nest egg by retirement age.

Capitalizing on government-offered savings benefits and seeking guidance can help you develop a solid retirement plan.

Everyday expenses often hinder saving efforts, but making retirement savings a top priority can pave the way for a more secure future.

Diversify Your Retirement Income

Diversifying your retirement income is a vital strategy to mitigate risks associated with potential changes in Social Security benefits.

- A well-balanced investment portfolio can help reduce the impact of market volatility on your retirement savings.

- A diverse investment in stocks, bonds, and real estate can provide a balance of growth and stability.

- Traditional and Roth IRAs provide different tax advantages, making them valuable tools for diversifying your retirement income.

- Additionally, stable income sources such as annuities can supplement Social Security, providing a steady income stream during retirement.

Maximize Employer Contributions

Optimizing employer contributions to your retirement plan is a simple yet effective approach. Many employers offer matching contributions to 401(k) plans, which can significantly boost your retirement savings.

Automating your retirement savings offers several benefits:

- Consistent contributions

- Takes full advantage of employer match opportunities

- Enhances your savings

- Provides tax benefits, such as tax-deferred contributions and lower taxable income

- Helps build a more secure financial future

Maximizing Social Security Benefits

Maximizing Social Security benefits is crucial for ensuring a secure retirement.

Delaying your retirement benefits until full retirement age or later is considered one of the most effective strategies for increasing your retirement income.

This approach can result in higher monthly benefit payments and a more secure financial future. Additionally, understanding and utilizing spousal and survivor benefits can significantly enhance your financial situation.

Strategically planning when to claim your Social Security benefits can make a substantial difference in your monthly payments.

Delaying Benefits

Postponing Social Security benefits can notably augment your monthly payments.

- If you start receiving benefits at age 62, your payment will be about 30% lower than if you wait until full retirement age, which is 66 or 67 depending on your birth year.

- Each year you delay receiving benefits between full retirement age and age 70 increases your benefits by approximately 8% per year.

- Waiting until age 70 to claim benefits can qualify you for delayed retirement credits, further boosting your monthly payments.

Spousal Benefits

Spousal benefits can provide significant additional income for those who qualify. A spouse can receive up to 50% of the primary earner’s full benefit if they claim at full retirement age.

To maximize spousal benefits, the higher-earning spouse can delay claiming their own benefits, increasing the amount the lower-earning spouse will receive.

Divorcees may also be eligible for spousal benefits based on their ex-spouse’s earnings, provided they meet certain requirements.

Survivor Benefits

Survivor benefits can be a critical source of income for widowed spouses. If your deceased spouse was eligible for a higher Social Security payment, you may qualify for a higher survivor benefit.

Survivor benefits can be up to 100% of the deceased spouse’s benefit if claimed at full retirement age or later.

Starting benefits before full retirement age can reduce both your benefits and the survivor benefits for your spouse.

The Role of Cost of Living Adjustments (COLA)

Cost of Living Adjustments (COLA) play a vital role in ensuring that Social Security and Supplemental Security Income (SSI) benefits keep up with inflation. COLAs are designed to offset inflation, helping retirees maintain their purchasing power as living costs rise.

Without these adjustments, retirees may struggle to balance their budgets on a fixed income due to the rising cost of living.

COLAs are determined based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) from the previous year’s third quarter to the current year’s third quarter.

Recent COLA Increases

Recent COLA increases have had a significant impact on Social Security benefits.

- The 2024 COLA increase for Social Security benefits is set at 3.2%, following an 8.7% increase in 2023, which was the highest adjustment in over four decades.

- These adjustments are calculated based on the CPI-W, ensuring that benefits keep pace with inflation.

- The latest COLA increase results in an average increase of $55 per check, benefiting nearly 67 million Americans.

Despite these adjustments, some critics argue that the CPI-W does not fully capture the cost increases felt by older Americans, particularly in areas such as health care and housing.

Future Projections

Future COLA adjustments are expected to continue, although their adequacy in countering inflation remains uncertain.

This uncertainty may affect the purchasing power of Social Security benefits, making it crucial for retirees to stay informed about potential changes and plan accordingly.

Engaging in in-depth research and staying updated on new projections can help retirees anticipate changes and adjust their financial plans to maintain their standard of living.

The Importance of Personal Retirement Planning

Get your retirement score today! In the face of uncertainties surrounding Social Security, personal retirement planning is of utmost importance now more than ever.

Early planning provides more time for investments to grow, leading to greater financial security in retirement. It also helps manage increasing medical expenses and ensures that you can maintain your lifestyle.

Personal savings and investments will take on a more significant role in securing financial stability in retirement, thus necessitating the exploration of diverse investment options and strategies.

Utilizing tools like the IFW Retirement Score can help assess your readiness and navigate potential uncertainties about Social Security.

Calculating Your Retirement Needs

Calculating your retirement needs is a crucial step in personal retirement planning.

Typically, you will need approximately 70% of your pre-retirement income to maintain your lifestyle in retirement. When calculating your needs, consider life expectancy and the risk of outliving your savings.

Checking your Social Security statement for errors can help ensure you receive the correct amount. By accurately calculating your retirement needs, you can create a comprehensive plan that supports your financial goals and provides peace of mind.

Using the IFW Retirement Score

The IFW Retirement Score is a valuable tool for assessing retirement readiness. This percentage-based metric evaluates the likelihood of meeting your income goals during retirement, considering various factors, including potential uncertainties about Social Security.

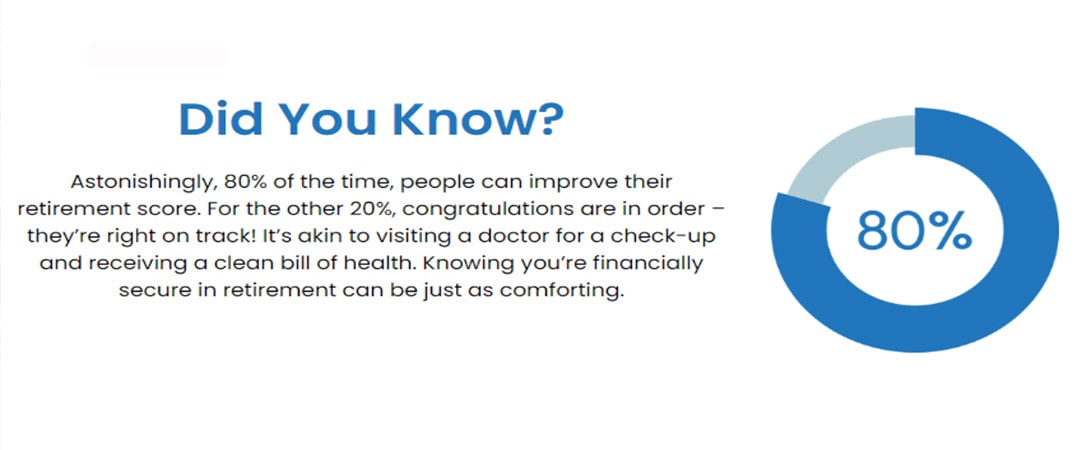

Calculated using Monte Carlo Simulation, a technique trusted by NASA for space missions, the Retirement Score provides a reliable assessment of your retirement plan’s success. By requesting your Retirement Score, you can discover ways to potentially reduce or eliminate taxes in retirement, protect your portfolio from market volatility, and secure a stable income stream. With 80% of people able to improve their retirement score, this tool can significantly enhance your financial planning.

Protecting Against Market Volatility

Protecting against market volatility is essential for maintaining financial stability in retirement. Doubts about Social Security benefits can prompt more cautious investment decisions. One effective strategy is to avoid risky assets and adopt more conservative investment options.

Opting for fixed-income investments, such as bonds, or stable assets like utility stocks and certain types of mutual funds, can reduce the potential impact of market downturns. By diversifying your investments and focusing on stable income sources, you can safeguard your retirement portfolio against volatility and ensure a more secure financial future. Some examples of stable income sources include:

- Government bonds

- Corporate bonds

- Dividend-paying stocks

- Real estate investment trusts (REITs)

- High-quality municipal bonds

By including these types of investments in your portfolio, you can create a more balanced and resilient retirement plan.

Summary

Navigating the future of Social Security requires a proactive approach and informed planning. Understanding the projected depletion dates, potential legislative changes, and their impact on benefits is crucial for all retirees.

Wealthy individuals, the middle class, and those nearing retirement must adopt tailored strategies to prepare for potential changes and maximize their benefits.

By starting to save early, diversifying retirement income, and maximizing employer contributions, retirees can build a robust financial foundation. Tools like the IFW Retirement Score can provide valuable insights and help individuals secure a stable income stream.

Ultimately, proactive planning and informed decision-making are key to navigating the uncertainties of Social Security and ensuring a secure retirement.

Frequently Asked Questions

What is the IFW Retirement Score?

The IFW Retirement Score is a percentage-based metric used to assess the likelihood of meeting income goals during retirement.

How is the Retirement Score calculated?

The Retirement Score is calculated using The IFWs proprietary algorithm, a reliable technique trusted by retirees and financial planners.

What can you discover by requesting your Retirement Score?

You can discover ways to potentially reduce or eliminate taxes in retirement, protect your portfolio from market volatility, and secure a stable income stream by requesting your Retirement Score. These insights can help you make informed decisions about your retirement planning.

Can you improve your retirement score?

Yes, 80% of the time, people can improve their retirement score, so there is a good chance you can do the same.

What is the purpose of the live webinar?

The live webinar aims to provide strategies to improve the chances of success in retirement. It offers valuable insights and information.

Related Articles

The Stages of Financial Life

As we transition through the various stages of life, our financial needs are also constantly evolving. The Institute of Financial Wellness examines the various stages of financial life and the

Evan Sussman

Oct, 25 2021

Traditional IRA vs. Roth IRA

Traditional Individual Retirement Accounts (IRA), which were created in 1974, are owned by roughly 36.1 million U.S. households. And Roth IRAs, created as part of the Taxpayer Relief Act in

Peter Foldes

Nov, 10 2021

Tax Efficiency in Retirement

Will you pay higher taxes in retirement? It’s possible. But that will largely depend on how you generate income. Will it be from working? Will it be from retirement plans?

Peter Foldes

Nov, 10 2021