“Retire from your job, but never retire your mind.” – Unknown

As a teacher, finding the best 403b for teachers plan is pivotal for your retirement security. In this opportunity, teachers, please take the desk and get ready to learn how to evaluate and rank the top 403b options, equipping you with the crucial information needed to make an informed choice. We’ll uncover which plans afford the best benefits and investments, minus excessive fees, to make your financial future as secure as your contribution to education.

Learn how the IFW Retirement Roadmap Experience Will Help You…Get There!

Key Takeaways

- It’s crucial for educators to select 403(b) retirement plans with low costs and passive investment options like ETFs and index funds and to be wary of high-fee plans.

- 403(b) retirement plans offer traditional and Roth contribution options, with tax advantages and potential employer contributions which may have more generous vesting schedules compared to other retirement accounts.

- Financial advisors play a critical role in assisting educators with selecting, managing, and minimizing the costs of 403(b) plans, and can act as 3(38) fiduciaries taking on investment decision responsibilities.

Honoring Educators: Teacher Appreciation Week and Retirement Planning

Teacher Appreciation Week is an annual celebration in the United States that recognizes the invaluable contributions of educators. Held during the first full week of May, this date provides an opportunity for students, parents, administrators, and communities to express gratitude for the hard work, dedication, and passion of teachers. This special week acknowledges the vital role teachers play in shaping the future and reaffirms support for the teaching profession. It’s a time for various activities, events, and gestures of thanks to celebrate how the teachers impact students’ lives and society. But beyond the heartfelt appreciation, it’s crucial for teachers to understand their investment options for a comfortable retirement.

Why is Teacher Appreciation Week Important?

Feeling appreciated and valued boosts teachers’ morale and job satisfaction. Happy and motivated teachers are more likely to go above and beyond to support their students, creating a positive learning environment conducive to growth.

In addition, teacher Appreciation Week provides an opportunity for students and teachers to strengthen their relationships. When teachers feel supported and recognized, they can better connect with their students, leading to better communication and collaboration.

Exploring Top 403(b) Plans for Educators

Educators seeking to build their retirement savings have access to a variety of 403(b) investment providers, each tailored to specific investment preferences. The Institute of Financial Wellness seeks to help teachers and individuals in general find the best strategy for managing their finances for a comfortable retirement.

These attributes lay down the framework for straightforward retirement planning while ensuring you have the necessary knowledge to make informed decisions about prevailing market conditions as well as offering numerous fiscal paths for consideration.

Nevertheless, educators within school districts should stay focused on selecting plans characterized by passive investments such as ETFs and index funds known for their low costs. They must also be wary of high-cost plans which sales agents may promote aggressively. Several states are taking action by passing laws requiring providers to clearly disclose all pertinent information concerning investments—a measure intended to help educators choose what’s genuinely advantageous for them.

Navigating Retirement Plan Choices in Higher Education

Choosing the right retirement plan in the sector of higher education involves more than just selecting an insurance company. It requires a grasp of the tax benefits and employer contributions associated with your 403 b plan. These plans permit you to make either traditional pre-tax contributions or Roth after-tax ones, providing advantages similar to those found in 401(k)s and IRAs. Varied policies may include matching contributions from employers that can enhance your retirement savings significantly, often coming with vesting schedules that are more favorable than other types of retirement accounts.

The array of investment products within 403(b) plans has broadened over time, moving past what was once primarily variable annuities on offer. It’s important to recognize that even though there is now greater diversity available for selection within these plans, they might not have as extensive a range as their 401(k) or IRA counterparts do. For individuals protected under ERISA – the Employee Retirement Income Security Act – there’s additional investor protection ensuring confidence while planning for retirement days ahead.

Within the realm of 403 b offerings by companies, fixed index annuities offered by an insurance provider stand out as distinct investment alternatives, delivering several compelling features.

- They allow participation in stock market upswings while shielding one’s initial contribution against potential downturns.

- There is potential for immediate returns reaching upwards to 12% offered as bonuses through contract life duration.

- The alignment process between one’s specific financial needs and their aspirations for growth paired simultaneously with protective measures ensures tailored strategies suitable towards securing future finances at times post-retirement.

The Role of Financial Advisors in Managing Your 403(b)

Navigating the complexities of a 403(b) retirement roadmap can often seem overwhelming, yet with the guidance of financial advisors, this process is made much simpler. Firms such as The IFW have acknowledged the importance of advisory services and urged their clients to embrace personalized counsel. Advisors are instrumental in easing the burden for non-profit entities by adeptly handling intricate aspects of 403(b) plans and maintaining adherence to evolving regulations.

At its core, advisors prioritize tailored financial planning and education to help reduce expenses associated with 403(b) accounts for educators while taking on investment choices as designated 3(38) fiduciaries. They offer support through every step—from picking appropriate funds at inception all the way through enrollment—equipping you with customized advice that aligns with your long-term ambitions and fiscal conditions.

Engaging a financial advisor presents several advantages.

- Simplification in managing retirement funds allows you more time devoted to what matters most – educating future minds.

- Their knowledge affords an opportunity for potentially higher profit from investments.

- Assurance comes from knowing there’s someone focused on protecting your economic interests throughout your professional journey into retirement.

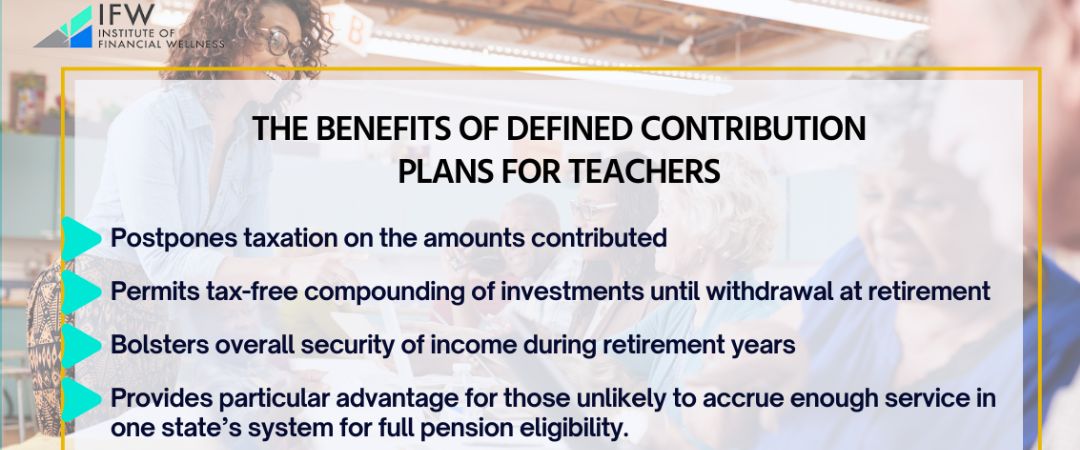

The Benefits of Defined Contribution Plans for Teachers

Defined contribution plans, including the 403(b), are specifically designed to meet the distinctive economic needs of educators. These plans offer a range of investment options and enable you to tailor your risk level based on your personal financial objectives and circumstances. The ability to transfer 403(b) plan funds without hassle if you switch employers or move between states is a key benefit, promoting professional flexibility while ensuring consistent growth for your retirement savings.

Contributing pre-tax earnings to a 403 b plan brings multiple advantages.

- Postpones taxation on the amounts contributed

- Permits tax-free compounding of investments until withdrawal at retirement

- Bolsters overall security of income during retirement years

- Provides particular advantage for those unlikely to accrue enough service in one state’s system for full pension eligibility.

The charm of defined contribution schemes such as the 403 b lies within their versatility—a capacity that allows them to adjust alongside life’s changes and fiscal ambitions—serving as an additional means beyond social security. For teachers who might be either initiating their contributions or experienced professionals fine-tuning their investment strategies, these plans constructively facilitate progress toward achieving substantial retirement reserves.

How to Maximize Your 403(b) Through Smart Investing

To maximize the potential of your 403(b) retirement plan, smart investing is key. High fees, such as management fees and costs associated with annuities, can eat into your retirement savings if not carefully considered. Therefore, it is crucial to take the time to research and understand the administrative costs and fees linked to your 403(b), as they can significantly impact your retirement profits.

When evaluating the funds available within your 403(b) plan, consider the following:

- Scrutinize the performance and fee structure of each fund.

- Prioritize low-cost funds to maximize your long-term financial outcomes.

- Diversify your investments across different countries and industries to mitigate risk and ensure a more stable return over the long haul.

Investing in your 403(b) isn’t just about putting away money for the future; it’s about doing so wisely. By paying close attention to fees, fund performance, and diversification, you set the stage for a retirement portfolio that’s as resilient as it is rewarding.

Simplifying the 403(b) Enrollment and Contribution Process

The enrollment and contribution process for 403(b) retirement plans, inclusive of payroll deductions, has been simplified to ensure that teachers can easily accumulate funds for their retirement. Typically, employees are entered into the plan with a preset contribution level by default but retain the option to modify this sum or fully opt out should they choose. When deciding on an appropriate amount to contribute toward your 403(b), it’s important to consider both the maximum annual pre-tax limit set at $20,500 as well as whether the standard savings rate is in harmony with your long-term retirement goals.

For individuals who are either over 50 or have dedicated at least 15 years of service, additional contributions beyond regular limits are permitted which serves as a means of bolstering their reserves for retirement late in one’s career [1]. Many providers also implement automatic increase features within these plans—these gradually increase your contribution percentage annually until reaching a predetermined goal, potentially enhancing your nest egg significantly over time.

Gaining clarity about how you enroll and manage contributions allows you greater control over ensuring adequate funds for later life. Whether through selecting optimal levels of investment now or leveraging incremental growth mechanisms offered by some plans, such as auto-escalation options—the decisions enacted presently could greatly influence financial stability during those golden years.

The Intersection of 403(b) Plans and Loan Forgiveness Programs

Educators considering retirement may discover that their planning could benefit from available loan forgiveness programs, which can significantly affect their financial strategy. The Public Service Loan Forgiveness (PSLF) program is one such initiative that offers to erase the remaining debt after 120 qualifying payments while employed by an approved employer. In a similar vein, educators who meet certain criteria and teach for five consecutive years in low-income schools might have up to $17,500 of their loans forgiven under the Teacher Loan Forgiveness program [2].

It’s crucial for teachers to recognize they must choose between these two programs. Simultaneous benefits are not permitted since one cannot use the same teaching service period towards both programs’ qualifications. Teachers should make this selection with a strategic eye on how each option fits within broader retirement strategies and personal financial goals.

For those navigating educator-specific financial landscapes, grasping the intricacies of such loan forgiveness schemes becomes integral when aligned with your 403(b) retirement plans. Thorough understanding enables more effective decision-making processes where every choice made furthers you towards achieving comprehensive fiscal objectives as you approach retirement.

Empowering Educators: Navigating Personal Finance with the Institute of Financial Wellness

In the realm of personal finance, educators don’t have to navigate their financial path solo. The Institute of Financial Wellness (IFW) provides a beacon for thorough financial education, equipping individuals with resources and services that enable them to make well-informed decisions regarding their finances. IFW distinguishes itself as an invaluable ally in reaching your fiscal objectives by delivering content that is both engaging and actionable while maintaining impartiality.

The IFW delivers consistent support through weekly webinars, retirement score analysis, and on-demand video content focusing on essential aspects of financial health, such as preparing for retirement, planning for college expenses, and understanding insurance options. Both the tailored IFW Retirement Roadmap and our educational programs are crafted to allow educators to aim high in envisioning their retirement years while protecting their assets from market fluctuations and undue taxes.

Opting for an association with an IFW Financial Professional involves teaming up with someone who understands that money-related choices are complex and require nuanced solutions. With access to more than 35 reputable certifications and accreditations across the network, you can rest assured that your journey towards financial enlightenment through the guidance provided by the IFW will be enriching as much as it is pleasurable.

Full Summary

As we close the book on our exploration of 403(b) plans for educators, remember that the right retirement plan is out there, tailored to your unique teaching journey. Armed with insights on provider options, the importance of financial advisors, and strategies for maximizing investments, you are now better equipped to navigate the path to a secure retirement. Whether you’re evaluating loan forgiveness programs or seeking comprehensive financial education through resources like the IFW, each step you take is a step towards a future filled with promise and peace of mind.

Frequently Asked Questions

What are the benefits of choosing a low-cost 403(b) plan provider?

Opting for a provider of a 403(b) plan with low costs can reduce the fees you pay, thereby enhancing the expansion of your retirement funds and ensuring that a greater portion of your money is invested in your future.

Such a decision could greatly influence your financial stability over an extended period, bolstering long-term security.

Can I contribute more to my 403(b) if I’m over 50 or have a long tenure in teaching?

Indeed, should you be over the age of 50 or possess an extensive career in teaching, you are potentially qualified for elevated contribution ceilings to enhance your retirement reserves through your 403(b).

Are there any tax advantages to enrolling in a 403(b) plan?

Indeed, by participating in a 403(b) plan, you can defer taxes on the money you contribute and also enjoy tax-free accumulation of investment earnings until you take out the funds, which is beneficial for retirement savings strategies.

How do loan forgiveness programs like PSLF or Teacher Loan Forgiveness impact my retirement planning?

Understanding the qualifications and how they integrate into your complete financial strategy is crucial for programs like PSLF or Teacher Loan Forgiveness, which can increase the amount of money you have available to put toward your retirement savings [3].

What kind of support does the Institute of Financial Wellness offer to teachers?

The Institute of Financial Wellness provides an array of tools for teachers seeking financial security, including personalized offerings such as the IFW Retirement Roadmap and webinars. Certified financial experts offer continual advice to support educators in reaching their retirement goals.

Related Articles

Traditional IRA vs. Roth IRA

Traditional Individual Retirement Accounts (IRA), which were created in 1974, are owned by roughly 36.1 million U.S. households. And Roth IRAs, created as part of the Taxpayer Relief Act in

Peter Foldes

Nov, 10 2021

Tax Efficiency in Retirement

Will you pay higher taxes in retirement? It’s possible. But that will largely depend on how you generate income. Will it be from working? Will it be from retirement plans?

Peter Foldes

Nov, 10 2021

Term vs. Permanent Life Insurance

According to industry experts, most people don’t have enough life insurance. LIMRA, which keeps close tabs on the industry, recently reported that average coverage equals $163,000, which is equivalent to

Peter Foldes

Nov, 10 2021