Term insurance is the simplest form of life insurance. It provides temporary life insurance protection on a limited budget. Here’s how it works:

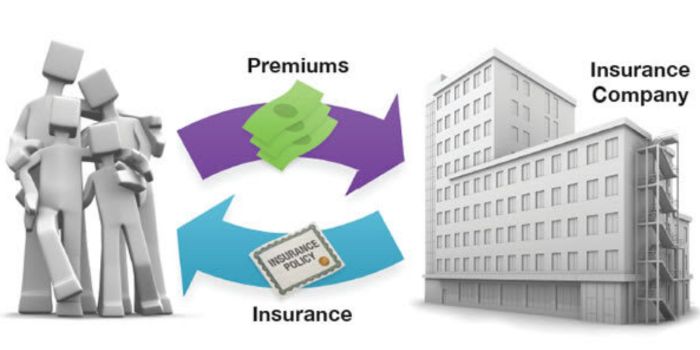

When a policyholder buys term insurance, they buy coverage for a specific period of time and pay a specific price for that coverage.

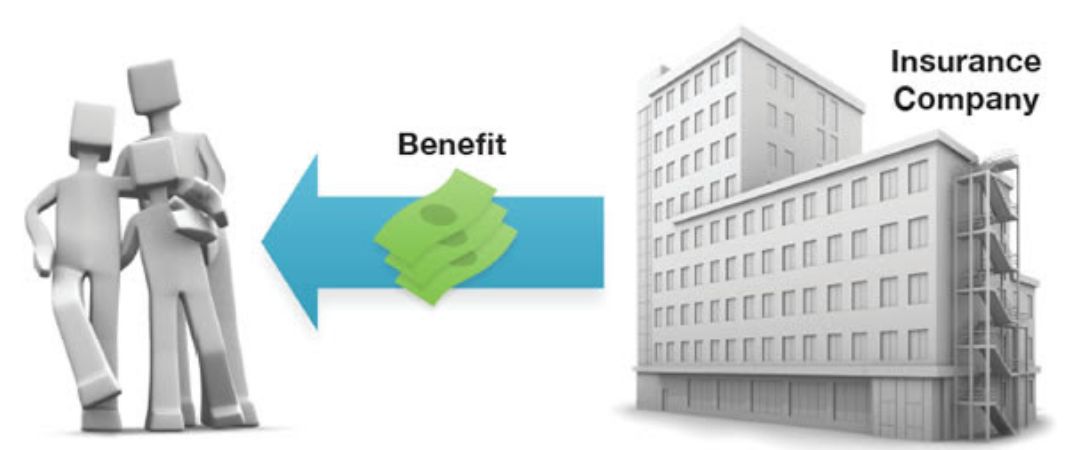

If the policyholder dies during that time, their beneficiaries receive the benefit from the policy. If they outlive the term of the policy, it is no longer in effect. The person would have to reapply to receive any further benefit.

Unlike permanent insurance, term insurance only pays. It does not accumulate a cash value. That’s one of the reasons term insurance tends to be less expensive than permanent insurance.

Many find term life insurance useful for covering specific financial responsibilities if they were to die unexpectedly. Term life insurance is often used to provide funds to cover:

- Dependent care

- College education for dependents

- Mortgages

Would term life insurance be the best coverage for you and your family? That depends on your unique goals, needs, and circumstances. You may want to carefully examine the pros and cons of each type of life insurance before deciding what type of policy may be the best fit for you.

Several factors will affect the cost and availability of life insurance, including age, health, and the type and amount of insurance purchased. Life insurance policies have expenses, including mortality and other charges. If a policy is surrendered prematurely, the policyholder also may pay surrender charges and have income tax implications. You should consider determining whether you are insurable before implementing a strategy involving life insurance. Any guarantees associated with a policy are dependent on the ability of the issuing insurance company to continue making claim payments.

Life insurance is not insured by the FDIC (Federal Deposit Insurance Corporation). It is not insured by any federal government agency or bank or savings association.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. This material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG Suite is not affiliated with the named broker-dealer, state- or SEC-registered investment advisory firm. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Copyright 2021 FMG Suite.

###

Learn More About IFW’s Life Insurance, Disability Insurance, and Long-Term Care Planning Services

What is your most valuable asset? The answer is you and your ability to earn income. This service is a must for anyone that wants to make sure they not only learn how to best protect themselves and their families but also discover meaningful benefits and best practices when it comes to insurance and protection.

- Find out what types of insurance make sense for your unique situation

- Learn how to determine an appropriate amount of coverage

- Pay the least expensive premium, while receiving the best value

- Discover how to use life insurance as a unique financial tool

- Plus, every participant will receive a free IFW Insurance Personal Report, including a review of all their current insurance and recommendations to improve their risk management program.

REGISTER HERE FREE FOR THE NEXT PROTECTING YOUR GREATEST ASSET LIVE WEBINAR

The IFW provides valuable financial education, resources, and services that help people live their best life.

Please remember, be mindful of the messenger that positions certain products or services as “always” bad or “always” perfect. The fact of the matter is there are no “bad products” or “perfect products”. The right product is the one that aligns with your goals and objectives.

The Institute of Financial Wellness believes when it comes to financial decisions; never say “Never” never say “Always”…It Depends.

Related Articles

The Stages of Financial Life

As we transition through the various stages of life, our financial needs are also constantly evolving. The Institute of Financial Wellness examines the various stages of financial life and the

Evan Sussman

Oct, 25 2021

Term vs. Permanent Life Insurance

According to industry experts, most people don’t have enough life insurance. LIMRA, which keeps close tabs on the industry, recently reported that average coverage equals $163,000, which is equivalent to

Peter Foldes

Nov, 10 2021

Consider Keeping Your Life Insurance When You Retire

Do you need a life insurance policy in retirement? One school of thought questions this decision. Perhaps your kids have grown and the need to help protect the household against

Peter Foldes

Nov, 10 2021